The Federal Reserve has mentioned time and time again they want the labor market to break, and they will only be pleased when the unemployment charge goes considerably larger than it is currently. This is why they continuously forecast a occupation-loss recession with their higher unemployment price forecast, and some Fed users chat about sending short-expression rates considerably larger. I a short while ago talked about this on CNBC.

Even although the headline inflation report was decrease than estimates, the 10-yr produce didn’t have much too a lot of a response these days. As I am composing this write-up, it’s trading at 3.42%.

While the 10–year yield, home finance loan fees and inflation appear about proper for my 2023 forecast, let’s not forget about the actual prize the Federal Reserve has in retail outlet: they want you to lose your work and that is why they maintain forecasting a job-loss economic downturn with a bigger unemployment rate.

Even though the Fed explained they are tracking main Individual Usage Expenditure (PCE) details above three, 6 and 12-thirty day period timeframes and their forecast shows that the data there should boost, it does not matter. The Fed is so frightened of the 1970s that the fear is extra crucial than everything else.

Even when they say rate hikes have a 12-18 thirty day period lag, indicating that the total impact of these aggressive fee hikes will not strike the economy until finally later on, they are not ready for that lag. They talk about extra rate hikes, and trying to keep fees better for for a longer time due to the fact they imagine this is the most productive way to defeat inflation — by generating extra labor provide through occupation losses. This is why they continue to do not care that housing is in a recession.

Let’s search at the interior details in this CPI report and come across some great nuggets to examine.

From BLS: The Consumer Price tag Index for All City Individuals (CPI-U) rose .1 per cent in March on a seasonally modified foundation right after expanding .4 p.c in February, the U.S. Bureau of Labor Data documented these days. In excess of the last 12 months, the all-objects index enhanced 5. percent prior to seasonal adjustment.

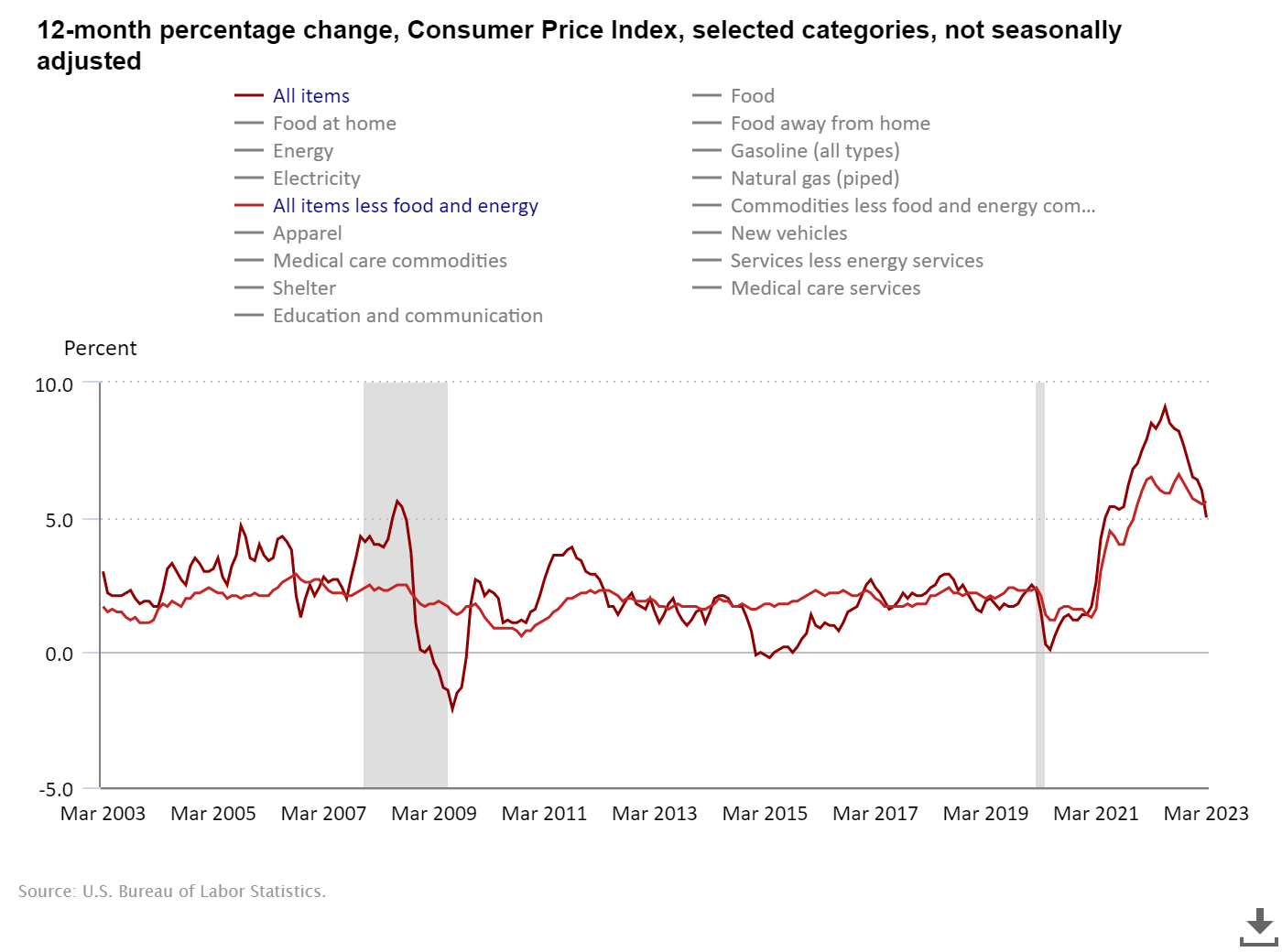

As we can see in the chart underneath, the year-more than-calendar year inflation advancement charge peaked a whilst again, and it’s tricky to drive this higher than the latest peak except if oil, food items, and hire take off once again.

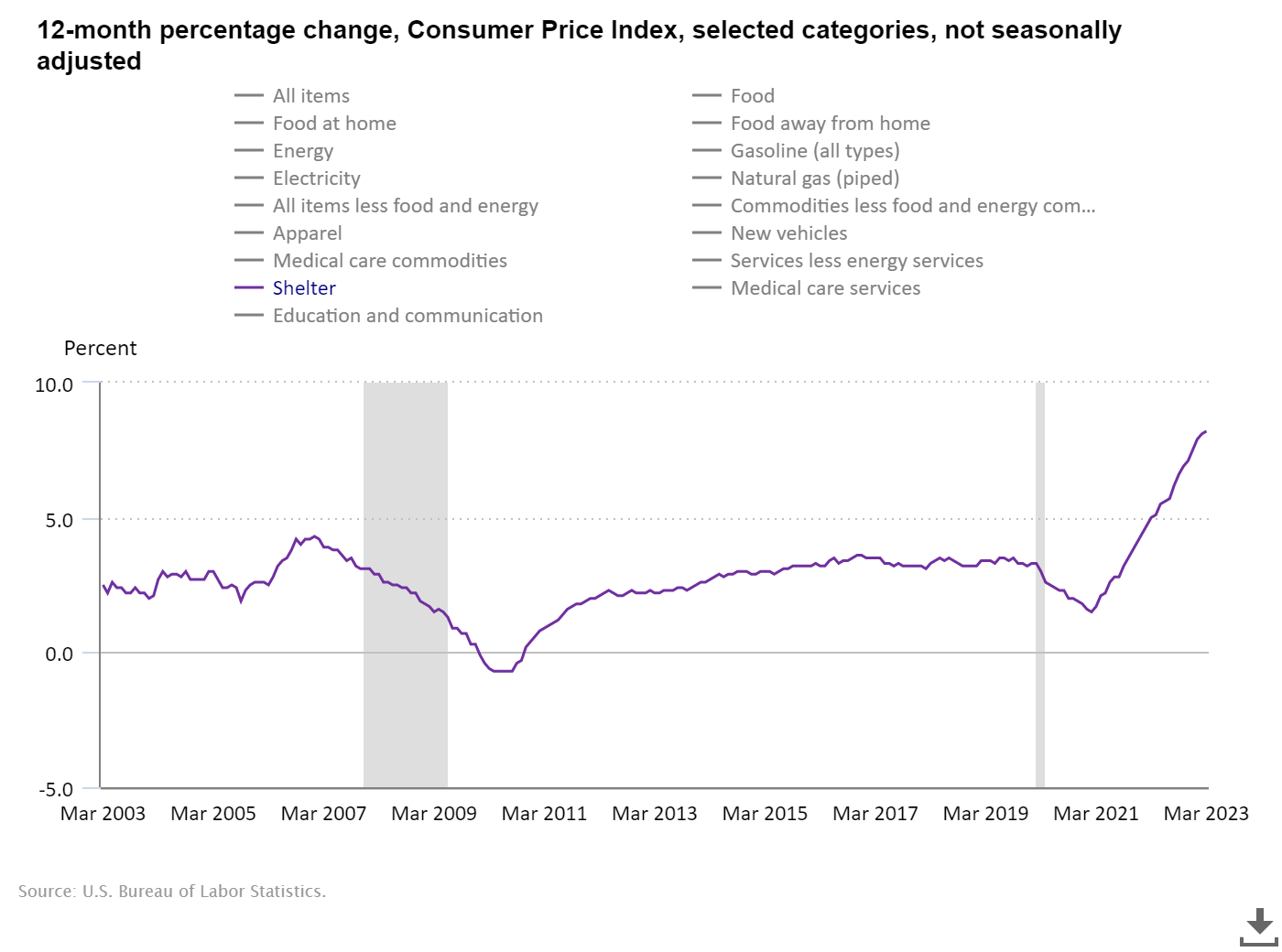

A person of the explanations did not see breakaway inflation during the housing bubble years is that lease inflation was tame again then. This hasn’t been the case a short while ago, and 44.4% of CPI is shelter inflation. We all know the lag of shelter in the CPI facts this is a thing I protected on CNBC previous September. I pressured that by January and February, we would see the progress level of shelter inflation fading, but it would take time to hit the CPI data.

We are having to the point where the calendar year-above-calendar year comps and the lag will start to display the progress charge of inflation declining and catching up with the recent current market truth, which implies the 1970s inflation thesis will endure nevertheless yet another blow.

We simply cannot have entrenched 1970s inflation due to the fact, back then, rental inflation was booming I indicate, it was large just before, and wage growth was scorching back again then much too. As you can see beneath, if shelter Inflation is about to begin its fact tour for the up coming 12 months, it will be tough to dance to disco audio yet again.

Also, in the past careers report, 12 months-over-12 months wage development is falling, all with a limited labor marketplace nonetheless.

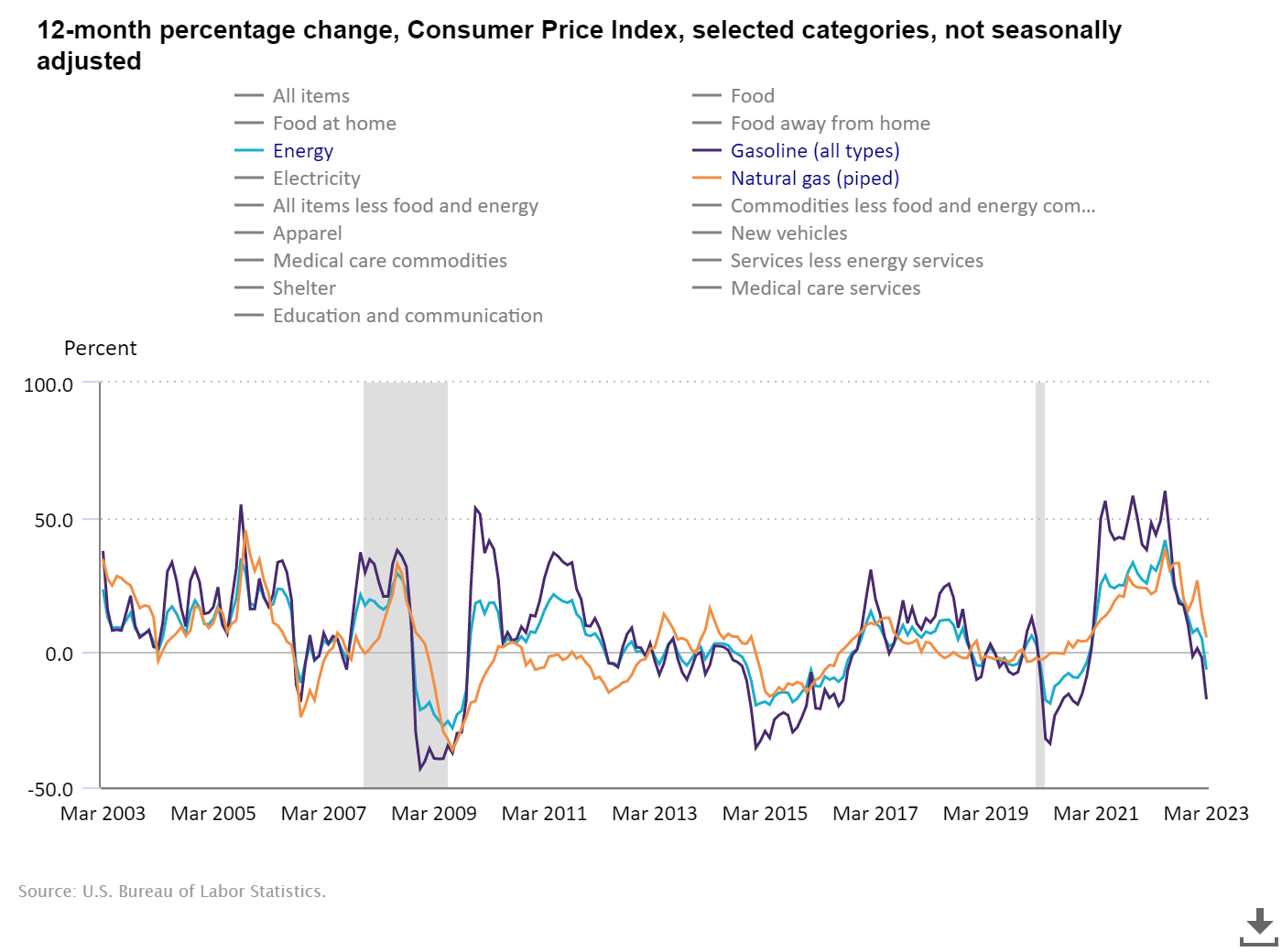

It’s tricky to get 1970s inflation except wage advancement, strength, food items and shelter all move a lot larger jointly, which is not going on. Electricity inflation is falling as the comps calendar year over calendar year are tough. The Russian invasion pushed strength price ranges a great deal higher.

We had higher oil prices from November 2010 to September 2014 with out CPI inflation breaking out simply because shelter inflation and wage growth had been tame back then. The chart under demonstrates the period of time I discussed with oil charges, when main CPI was very tame.

Even nevertheless the CPI inflation info came in lower than expected on Wednesday, we saw no substantial drop in the 10-year generate. House loan pricing did get a tad better this morning, as the past two days’ pricing was really negative.

With the 10-calendar year produce continue to investing in the 2023 forecast assortment of 3.21%-4.25%, the bond sector has acted remarkably in line with my check out that everyone is waiting for the labor marketplace to crack, primarily the Federal Reserve, prior to we make yet another intense move reduced in the 10-12 months produce.

We all know that shelter inflation will fade about the up coming 12 months, earning it mathematically not possible to have one more burst in inflation. The housing current market wants bond yields to go down and the spreads amongst the 10-12 months generate and 30-12 months property finance loan level to get improved to get a lot more traction.

Order application details also arrived out on Wednesday and it was beneficial 8% week to week, which indicates 2023 so significantly has experienced more constructive purchase software information than unfavorable.

Now, picture a housing marketplace with home loan prices in the small 5% array, not in the mid 6% vary. That would transform a ton of the dynamics in the housing marketplace and put the sector on more solid footing. Even so, until then, we will track all the economic data just one working day and a single week at a time.