Incentivized by a 200 foundation stage decline in home finance loan prices, 14 million householders in America refinanced their mortgages concerning the second quarter of 2020 and the fourth quarter of 2021, according to a current research report by the New York Fed.

Approximately 5 million home owners extracted $430 billion in dwelling fairness from their funds-out refinancings ($81,000 on normal), though 9 million received a fee-phrase refi and shaved far more than $200 on ordinary from their monthly mortgage loan payments.

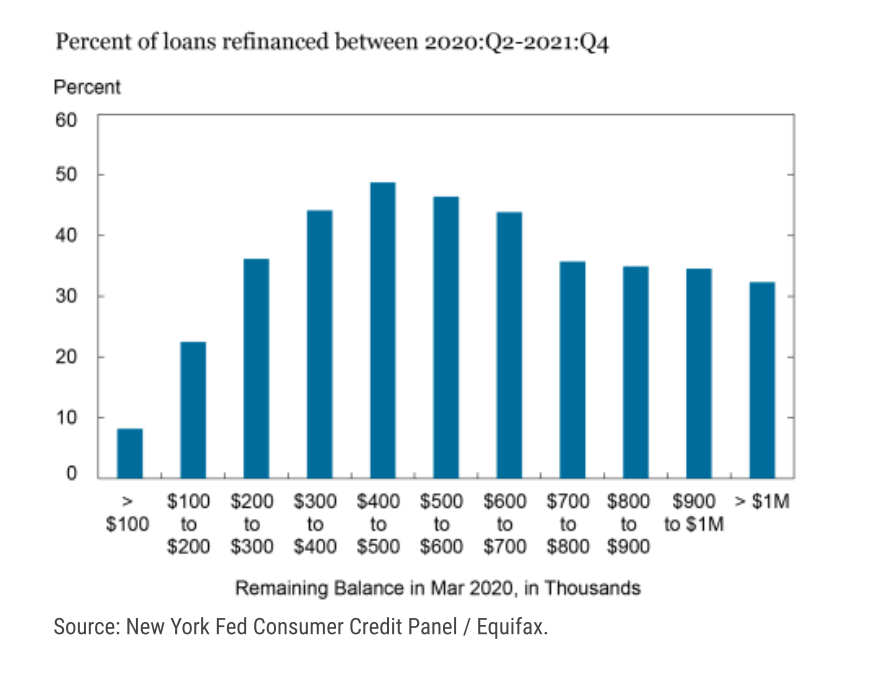

All told, around a person-third of fantastic mortgage balances bought refinanced for the duration of the refi boom, and an extra 17% of home loans exceptional had been refreshed by means of home gross sales, the New York Fed identified.

In other text, 50% of home owners with a home loan in The usa have minimal monetary incentive to offer. They are actually disincentivized given that they’d experience a housing market place where by dwelling prices are 36% greater than they had been pre-pandemic and the price tag of financing is up considerably.

It seems significantly very likely that the COVID refi boom will establish to be the most consequential celebration in housing in present day American background. It reset the board. Property finance loan lenders have been so effective at refinancing their own clients that they have a vastly diminished purchaser base just two yrs afterwards. Some loan companies won’t endure. Authentic estate brokerages have a connected issue — transaction volume is down. Way down. Their bread-and-butter go-up shoppers cannot make the math operate and/or are reluctant to give up what they’ve bought.

Acquire my wife’s cousin Christopher, for case in point. Christopher and his spouse acquired a townhouse in Charlotte, North Carolina, in 2021 and scored a mortgage loan charge in the 2.8% variety. They want to start off a family before long and would like extra area and garden, but come to feel caught. They don’t want to give up that house loan fee. Despite the fact that they could hire out the townhouse and make a revenue, it wouldn’t be more than enough to offset the expense of a new residence in the suburbs.

At this issue, Christopher is waiting right until a key existence celebration happens or the industry results in being significantly far more favorable.

A whole lot of homes are in this sort of keeping sample. In a current study by Realtor.com, 82% of 1,200 probable sellers felt “locked in” by their currently lower mortgage fee.

So wherever do housing execs change? There is constantly the initial-time homebuyers who are prepared to acquire the leap. And a proportion of people will move for new work opportunities, divorce, death of a husband or wife, and many others. But the actuality that most residence sellers also need to invest in at the exact time complicates issues and will suppress transaction volume right until affordability enhances.

The medium-term solution may relaxation with the boomers (due to the fact they have all the dollars). In that aforementioned Real estate agent.com survey of opportunity sellers, much more than half of these who recognized by themselves as boomers said they did not come to feel “locked in” by their recent home loan level. (It’s really worth noting that 87% of Gen Xers reported they did feel locked in, but one particular-third mentioned they planned to offer anyway, perhaps for the reason that they have lessen personal debt levels.)

A similar possible target is the roughly 40% of households that really do not have a mortgage loan and individual their assets “free and crystal clear,” according to Census Bureau knowledge. This group tends to be older and must prepare out their remaining chapter in life. That may well suggest going to be nearer to family and downsizing, extracting equity from their household to shell out for age-in-spot upgrades (HELOCs and reverse mortgages), or locating a extra cost-effective life style in a cheaper spot. If we’re likely to see stock unlocked, this is a single section it will have to occur from.

Where do you imagine current home stock will appear from? And when? Share your ideas with me at [email protected].

In our weekly DataDigest publication, HW Media Controlling Editor James Kleimann breaks down the largest stories in housing through a details lens. Indication up here! Have a topic in mind? Electronic mail him at [email protected]