On Tuesday the FHFA Home Value Index strike an all-time significant. In this post I’ll clarify why this is occurring and why we still have a savagely unhealthy housing market place. The swift takeaway below is that total active listings in the U.S. are nonetheless close to all-time lows and the demand has stabilized.

If household revenue had been crashing at the exact pace they were being past calendar year, we would all be getting a various dialogue. This is why I have stressed that Nov. 9, 2022, was an inflection level in housing. It’s not for the reason that need has rebounded in a huge way, it is just that household income stopped collapsing as they did in 2022.

Ahead-looking housing facts flipped in November, so HousingWire produced the weekly Housing Market Tracker to supply real-time forward-seeking housing details. I also not too long ago joined Mike Simonsen’s Leading of Thoughts podcast to discuss about what is transpired in housing more than the previous year. Forward-searching housing data may possibly not be pretty, but it functions.

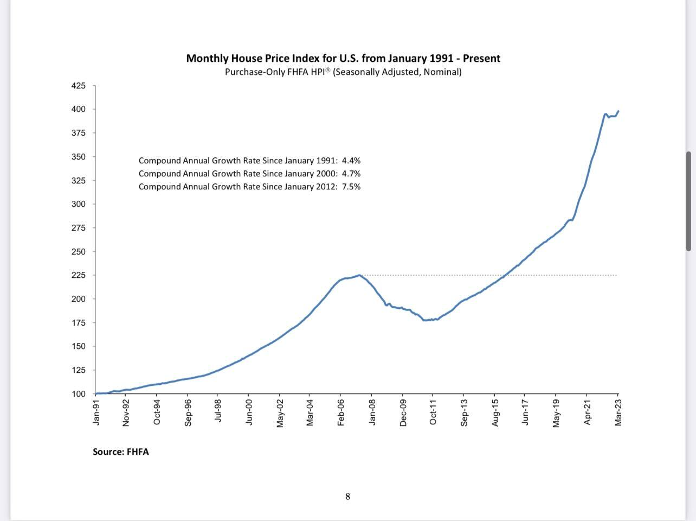

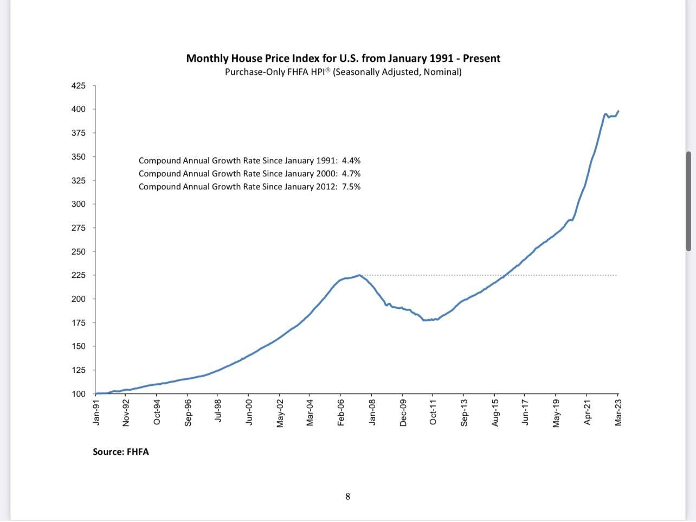

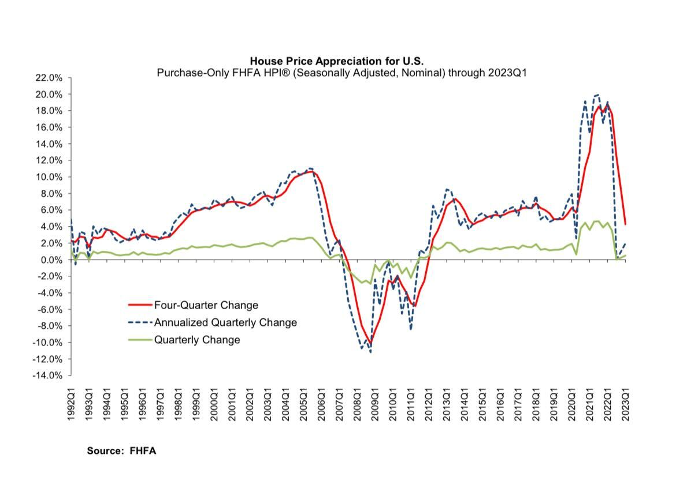

From FHFA: U.S. property charges rose 4.3 percent in between the first quarters of 2022 and 2023, according to the Federal Housing Finance Company Household Rate Index (FHFA HPI). Dwelling charges ended up up .5 percent compared to the fourth quarter of 2022. FHFA’s seasonally altered regular monthly index for March was up .6 p.c from February.

How and why did the index access this large, and what ought to we assume in the foreseeable future?

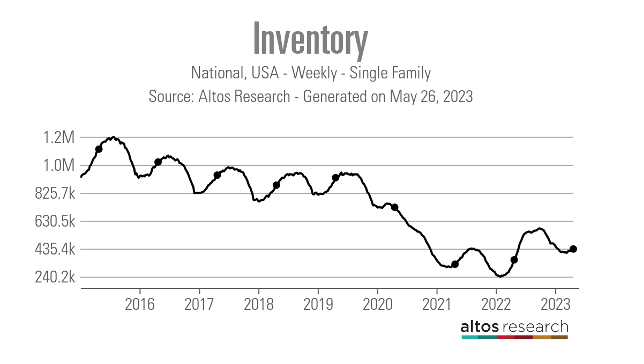

Stock is however in the vicinity of file lows

The easiest financial dialogue right now is the housing inventory story in the U.S. and that it is historically very low. Even so, it’s also the most-lied-about subject matter in new financial historical past. Individuals assert inventory is not minimal because “shadow inventory” is on the verge of including tens of millions of residences into the marketplace any next now. A different fantasy is that we’ll have a silver tsunami exactly where just about every Toddler Boomer lists their home in 1 thirty day period, flooding the marketplace with stock.

The NAR full lively listings data is between 2 million and 2.5 million in a standard sector concerning 1982-2023. Post COVID-19, we broke to all-time lows and it is challenging to get it back to those degrees: we’re presently at 1,040,000 lively listings. This is a simple fact that some folks have a tough time believing due to the fact they consider the shadow inventory or vacant house thesis.

These are typically middle-age male stock traders or any one from the anti-central bank movement who has been part of a borderline ridiculous bearish American economic crash squad that only can be matched by the Russian troll motion spreading disinformation about the state of the U.S. economic climate. Economic cycles occur and go, but the 24/7 doom porn people are a 1-trick pony that will drop into the grave with all American bears who have failed since 1790.

NAR whole stock considering the fact that 1982:

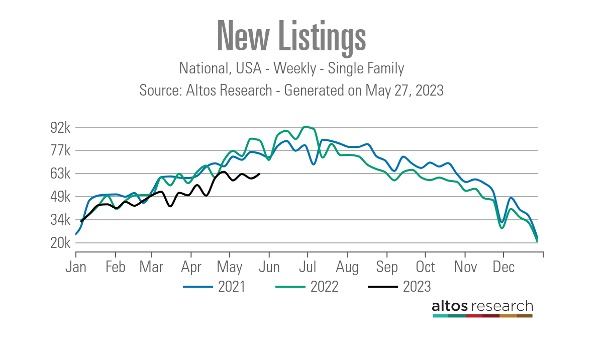

I favor the Altos Analysis weekly one-loved ones data to the NAR details simply because it presents us a clean glance at not only active listing facts but new listing data. This way, no person can be stunned when previous stale knowledge comes to the marketplace. This is also why we designed the weekly Housing Industry Tracker posting. We want to join the dots with provide and demand from customers.

The Altos Investigation new listing facts is important in monitoring the source factor of housing, which is why I consist of it as section of the Tracker. Even in 2022, when we had the most important household income collapse at any time recorded, the new listing knowledge never exploded bigger in simple fact, it was trending at all-time lows in 2021 and 2022, and now is at a new all-time small in 2023.

The data in the charts higher than really should clear up any shadow stock and vacant home nonsense we have read for in excess of 11 yrs. Let us speak about the 2nd considerable factor: desire!

Final 12 months was a whirlwind for housing economics. The to start with three months of 2022 had been so bad that I considered it the unhealthiest housing current market put up-2010. I coined the term savagely harmful because we experienced far too numerous people today chasing too couple of residences. A lot more than 70% of the market noticed many bids on properties.

In February of 2021, I talked about how we necessary bigger premiums to cool down the housing sector since this was not the housing bubble of 2005. Having said that, by February 2022, it was way too late so substantially residence-price tag expansion in such a shorter time meant that desire would collapse when mortgage loan prices did rise.

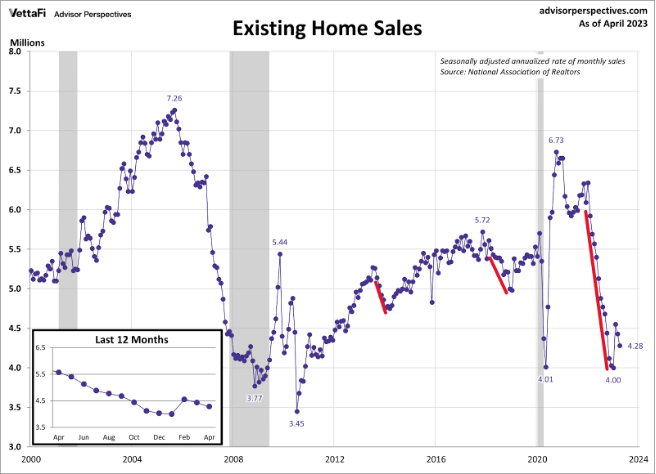

Mortgage loan costs likely from 3% to 5% experienced been the norm for the marketplaces mortgage prices going from 3% to 7.37% was a further story altogether. As a consequence, dwelling profits collapsed in 2022 in the most distinguished style at any time recorded in U.S. record.

So what has changed? Very well, starting off Nov. 9, 2022, home loan costs fell and house loan demand acquired much better. We didn’t see a restoration in need, it just stabilized.

Since Nov. 9, acquire application facts has had 17 constructive prints versus 9 negative prints just after creating some holiday getaway changes. Year to day, we have experienced 10 positive prints and nine negatives, and tomorrow buy programs should really be negative, which exhibits the stabilization in demand from customers so much in 2023.

It is easy supply and desire economics. Very last yr, house profits crashed because home loan charges exploded bigger after the most sizeable small-phrase household-rate gains at any time in background. Nonetheless, just after Nov. 9, that truth improved from crashing household product sales to stabilizing.

So the ethical of the story is that the current market dynamics have been extremely historic past 12 months energetic stock and month-to-month supply ended up minimal, but dwelling product sales have been crashing, and the inventory that was on the market, particularly in the seconnd 50 % of 2022, necessary price tag cuts to offer.

In my 2023 forecast for prices, I stated that home finance loan prices wanted to remain increased, over 5.875%, for costs to have a mild drop, in contrast to the significant rate gains we have viewed in 2020 through 2022. I selected 5.875% due to the fact my affordability index model was shot, but I also saw that the housing marketplace transformed when costs moved from 7.37% to 5.99%.

Picture what the housing details would look like if rates have been in the small 5% for 2023. This is why tracking weekly housing data is critical. We really don’t have a housing desire restoration as we noticed with the COVID-19 restoration, we just have a stabilization in demand, and full energetic listings are nevertheless close to all-time lows.

As you can see in the FHFA property selling price index underneath, the progress price of rates cooled down a lot with larger house loan fees, but all those did not crash price ranges like in 2007 and 2008, a period of time in time with a lot better active offer.

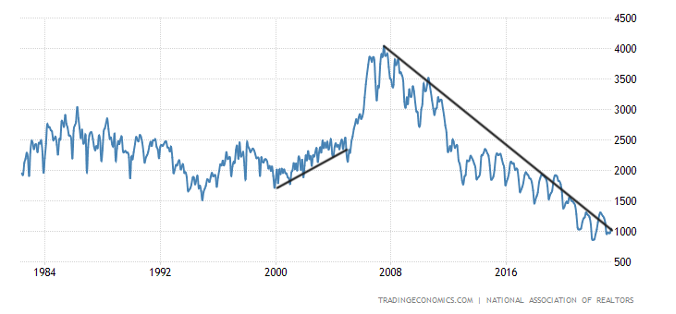

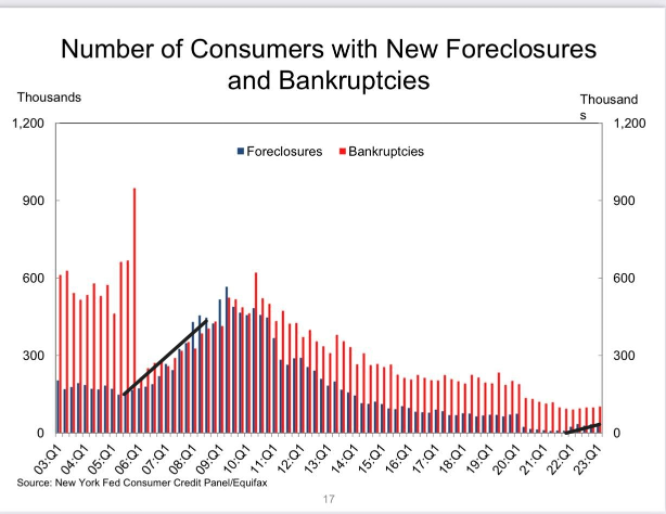

Also, to go along with the FHFA dwelling value index, not only was housing inventory in excess of 4 million in the NAR data in 2007, but we also had substantial growth in pressured sellers. As we can see in the chart under, we had large credit score anxiety in the method.

So, as we get prepared for the second fifty percent of 2023, we will track the weekly housing data. We will emphasis on the precise information that make any difference, constructive or destructive. The most major change this 12 months is that house gross sales are not collapsing in the exact same fashion they had been last year.