So, we can now incorporate a new variable into the equation for 2023: What does a banking crisis suggest for house loan rates?

In my 2023 forecast, I reported that if the economic climate stays firm, the 10-year yield selection need to be among 3.21% and 4.25%, equating to mortgage loan premiums of 5.75% to 7.25%. If the economy will get weaker and we see a rise in jobless claims, the 10-year yield really should go as small as 2.73%, translating to 5.25% home finance loan charges. This assumes the spreads are large as the property finance loan-back securities sector is continue to quite pressured.

The financial facts was Alright final 7 days. If we did not have the banking disaster, we would likely just focus on how company the financial knowledge was very last 7 days. GDP advancement was estimated at 3.2%, jobless statements fell past week, housing starts conquer estimates and buy application facts showed some progress. Retail revenue were slightly underneath estimates, but we had optimistic revisions, and industrial generation was unchanged.

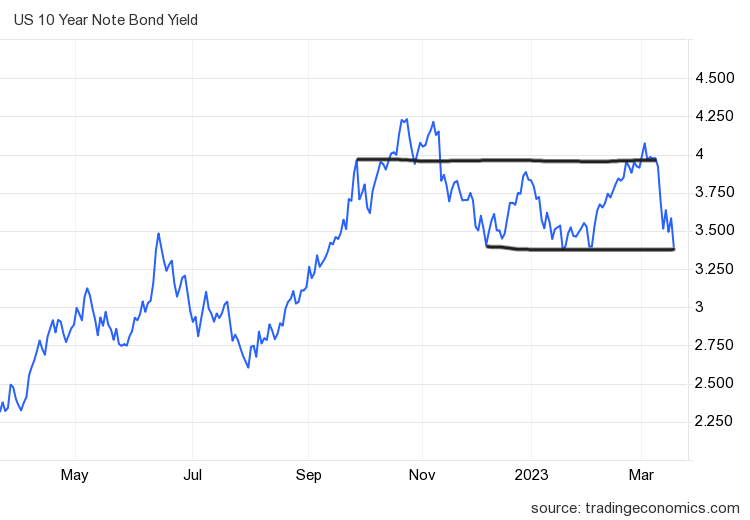

Very last week’s 10-calendar year produce took us to the important line in the sand.

Past 7 days the two-12 months produce collapsed from a 5% amount to below 4%. This bond market is screaming at the Fed to slash fees. On the other hand, quite a few Wall Road companies had been betting on increased premiums and acquired burned by the banking crisis. So, the sector is wild and the Fed could possibly not care what quick-term costs are accomplishing now.

Property finance loan prices fell and finished the week at 6.55%, even so, we see a whole lot of stress in the money markets. Many men and women questioned why house loan premiums weren’t lessen on Friday the respond to is that the banking crisis has stressed the mortgage loan-backed securities current market more than when bond yields fell to these amounts last time.

So this is likely to be an epic week for the reason that we have integrated a new variable into 2023 that was not in the equation at the commence of the yr and the Fed satisfies on Tuesday and Wednesday.

I want to see how the 10-12 months yield acts this week. Can we get follow-by means of bond buying, which would choose a direct shot at the reduced-amount assortment of 3.21%? That would be a big offer to me due to the fact it is happening with the labor marketplace even now carrying out Ok.

We really don’t know what information can happen at any second to change the landscape of the economic discussion until eventually the economical marketplaces quiet down.

With the possible of news having worse in the shorter expression, we have to have to be conscious that we can see some crazy current market pricing in property finance loan rates and moves in the 10-year generate. So, each individual working day counts now all through a banking crisis, as the planet marketplaces are trying to restore some buy.

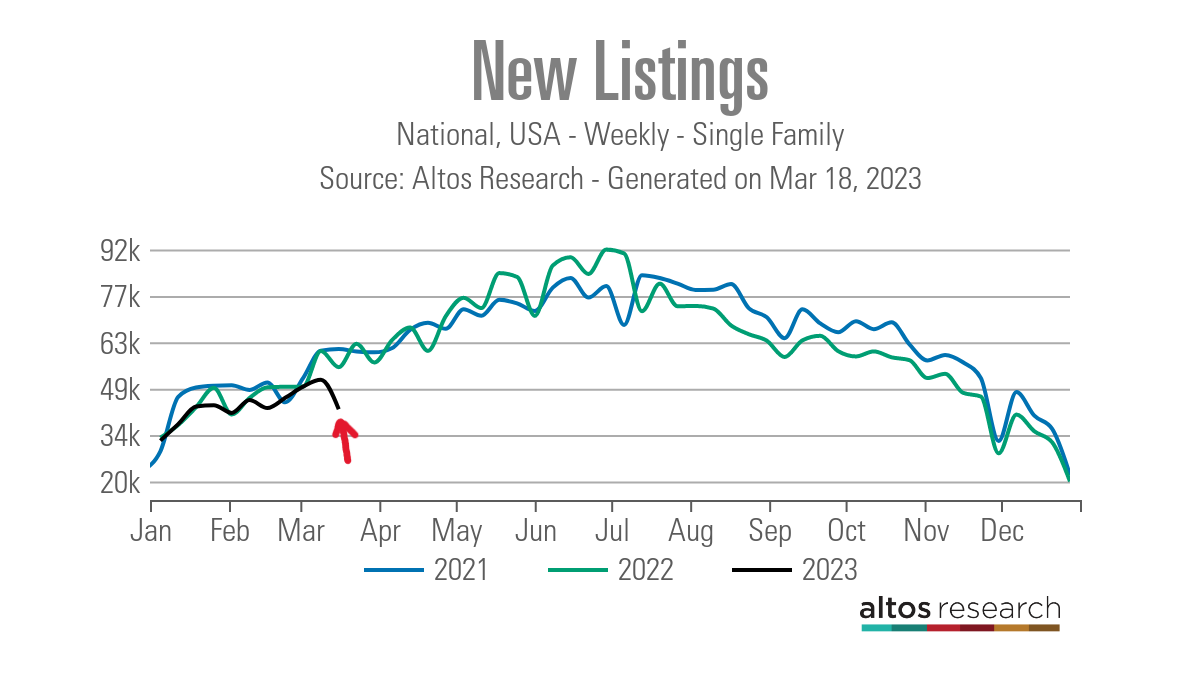

Weekly housing inventory

Searching at the Altos Investigation info from past 7 days, the significant query is no matter whether we are last but not least commencing to see the seasonal improve in spring stock. On this entrance we have some good news and some negative news.

1st, we noticed a somewhat amplified amount of lively listings, which designed me soar for joy! Past March is when we saw the seasonal base ahead of inventory took off, so I am hoping we get the exact progress in the data this 7 days, building it again-to-back years that we bottomed out in March. Although which is not ordinary, it’s much better than what we noticed in 2021 when we did not hit base until finally April.

- Weekly stock adjust (March 10-March 17): Rose from 412,535 to 414,278

- Same week very last year (March 11-18th): Fell from 247,320 to 245,776

- The bottom for 2022 was 240,194

The seasonal improve in stock usually means additional sellers can also be consumers of households and much less bidding wars in specific pieces of the country.

Now the negative news: new listing information fell so considerably this 7 days that I am placing an asterisk on this week’s info right until we see if this is a trend or just a one-off in the weekly data that can arise from time to time.

Also, we are generating a bigger hole in the 12 months-above-yr info. Previously in the 12 months, we ended up on par or even a bit bigger some weeks than the preceding two yrs. Now we are producing a more substantial hole, as you can see down below:

- 2021 60,904

- 2022 55,348

- 2023 42,407

For some historical reference, these were the weekly inventory information in past decades:

- 2015 80,909

- 2016 84,647

- 2017 78,237

Now, this new listing quantity can be a person 7 days of knowledge that just reverts to the craze, which would be larger than this amount. Or, like last 12 months at the conclusion of June, when charges spiked better, we saw a recognizable decline in new listings, given that homes did not want to listing their households with costs climbing.

This is anything that I have talked about ahead of — some householders just don’t want to acquire households with house loan rates of 7% plus and decide to get in touch with it to quits. This is a dilemma when home finance loan charges transfer higher much too rapidly, and it gets harder to make that massive lifetime-prolonged determination when the expense of housing matters.

Let us wait around two more months and see if this new listing trend carries on or just reverts higher. I am hoping it is just a one-week event.

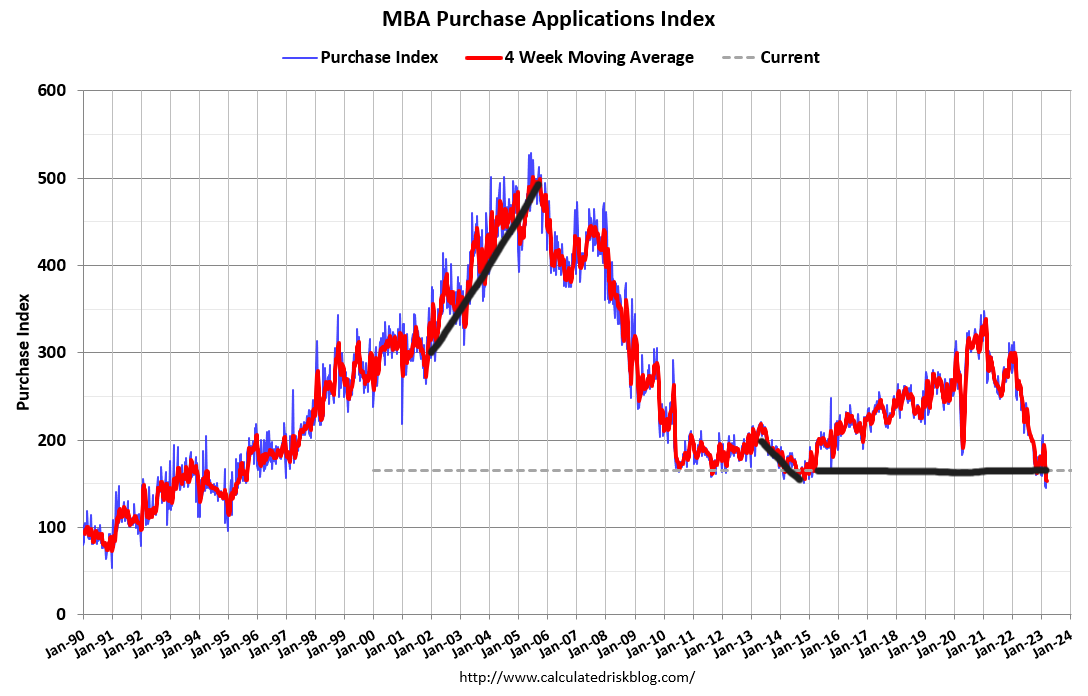

Purchase software data

Past week we bought superior news with one more 7% week-to-week gain on purchase apps, and the yr-more than-yr drop also fell. Having said that, as I usually tension, the bar is lower below, so it does not get substantially to go the needle on software data when property finance loan prices move lower.

When costs spiked from 5.99% to 7.10%, that gave us a single month’s negative information week to 7 days, but the final two weeks have been constructive. We have experienced a lot more positive invest in software knowledge than damaging considering the fact that Nov. 9. Considering that this details seems to be out 30-90 times, this week’s present house sales report need to see a bounce.

We need to be aware of the information coming out later on in the 12 months with the a single-month decline in this index. Even so, you don’t have to have to be a rocket scientist or have a Ph.D. in economics here to realize the housing current market is going with wherever the 10-12 months yield is heading, even with home finance loan spreads wide. So with all the drama we have currently, let’s see if mortgage charges tumble even further this week or whether the line in the sand holds.

The 7 days forward

This 7 days we have existing property product sales and new house profits experiences coming out, but to be dead trustworthy, economic data doesn’t matter until we get management of this banking crisis predicament. While creating this posting, information broke that UBS is getting Credit score Suisse with federal government assist and Flagstar will invest in Signature Financial institution property. In addition, the Fed introduced a

coordinated central bank motion to improve the provision of U.S. greenback liquidity.

In situations like this, marketplace drama requires to calm down first ahead of we can emphasis on the economic info. The Federal Reserve will meet up with this week on Tuesday and Wednesday, and the Q&A portion of this meeting will be epic.

Remember that back in November Fed Chair Powell stated, “I never have any sense we have overtightened or moved far too rapid.” Now, just after all the crisis banking lending packages and worldwide coordination to hold the banking technique operating, does he continue to believe this statement? I am hoping someone asks him this direct query.

Listening to what the Fed states this week is crucial. We can aim right on the housing information, but the noise this week will ascertain regardless of whether the current market thinks this banking disaster is beneath management or it’s burning out of regulate, forcing the Fed and the governing administration below and all around the environment to do a lot more to tranquil the marketplaces down.