Not only has the knowledge stayed organization, but the financial data has enhanced not too long ago.

Also, fuel charges are down from the peak, and the inflation progress charge is no longer skyrocketing. If the labor market place breaks this calendar year, which means jobless statements significantly increase, that should send out the 10-yr generate to 2.73%, and mortgage loan charges can go as very low as 5.25%.

Jobless statements have been stable for some time, and this is a major cause why I do not believe that the Federal Reserve is going to pivot outside of this. They often produced it very clear they want the labor market to break, so go with that premise until they say or else.

Housing permits will drop all calendar year, but revenue picked up just lately, a optimistic for the economy, that means more transfers of commissions. An enhancing financial system puts more hazard to the upside in premiums and bond yields, primarily if inflation details picks up.

If the reverse was going on, economic data would get weaker with much less intake and additional persons submitting for unemployment claims. Fees should really fall because, as opposed to in the 1970s, lessen economic advancement and fewer jobs should really not make far more inflation as it did in 1974.

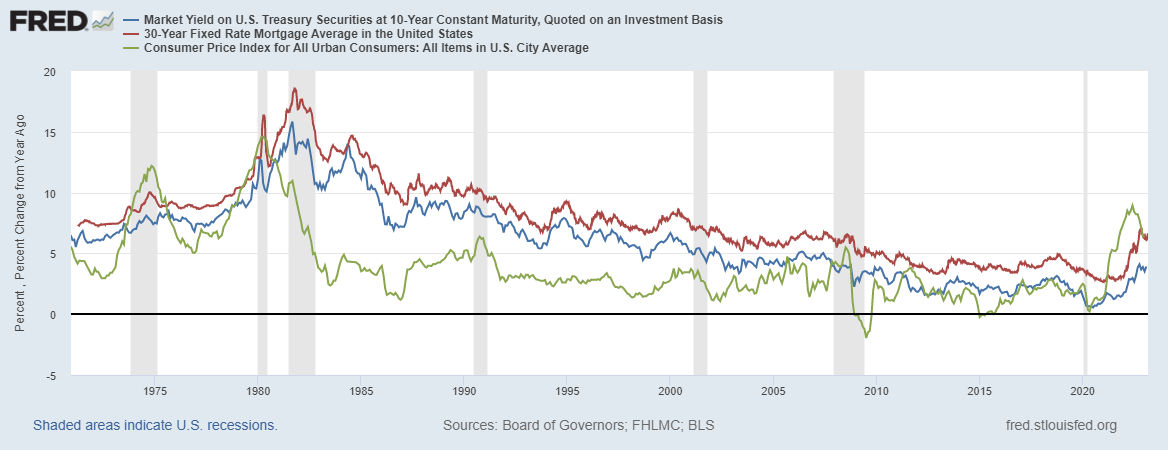

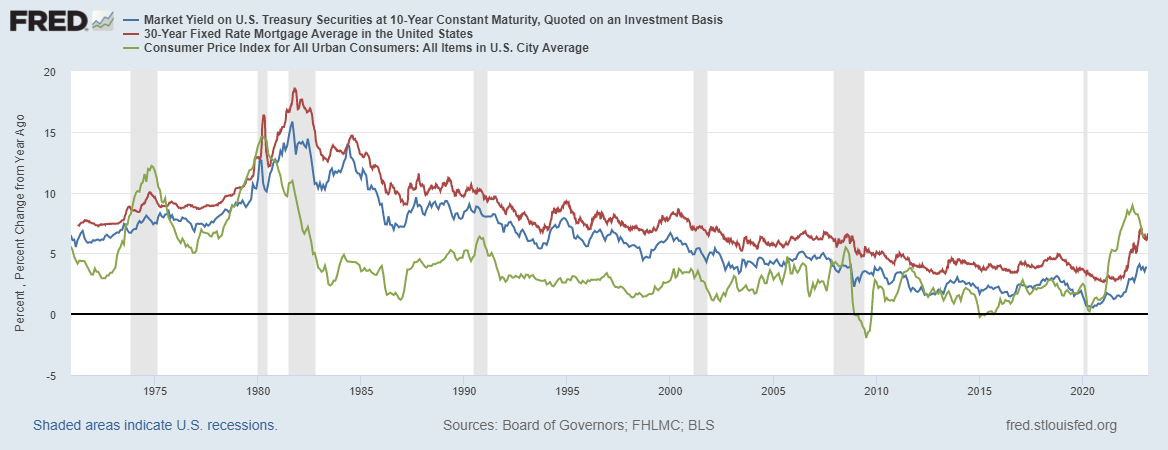

It’s true that inflation is booming like we have not viewed since the 1970s, but the truth is that if the bond industry thought in entrenched inflation, it would have been pricing the 10-year generate considerably greater around the previous 12 months.

CPI inflation took off a few moments in the 1970s, alongside with house loan costs and the 10-year produce. Now inflation has taken off all over again, but property finance loan prices have nonetheless to get higher than 8% as we observed in the mid to late 1970s, and the bond sector has also not damaged over 5.25% on the 10-year generate. Also, the Federal Reserve isn’t speaking about having the Fed Money amount again to late 1970 concentrations possibly.

Housing in the 1970s was booming!

Have you at any time questioned why the Federal Reserve mentioned we required a housing reset in March 2022 but not a labor market place reset? They’re targeting the labor sector in the feeling that if additional People in america eliminate their employment, we will have extra supply of personnel, which will lead to much less wage progress and significantly less inflation. However, they didn’t use the word reset regarding the labor industry.

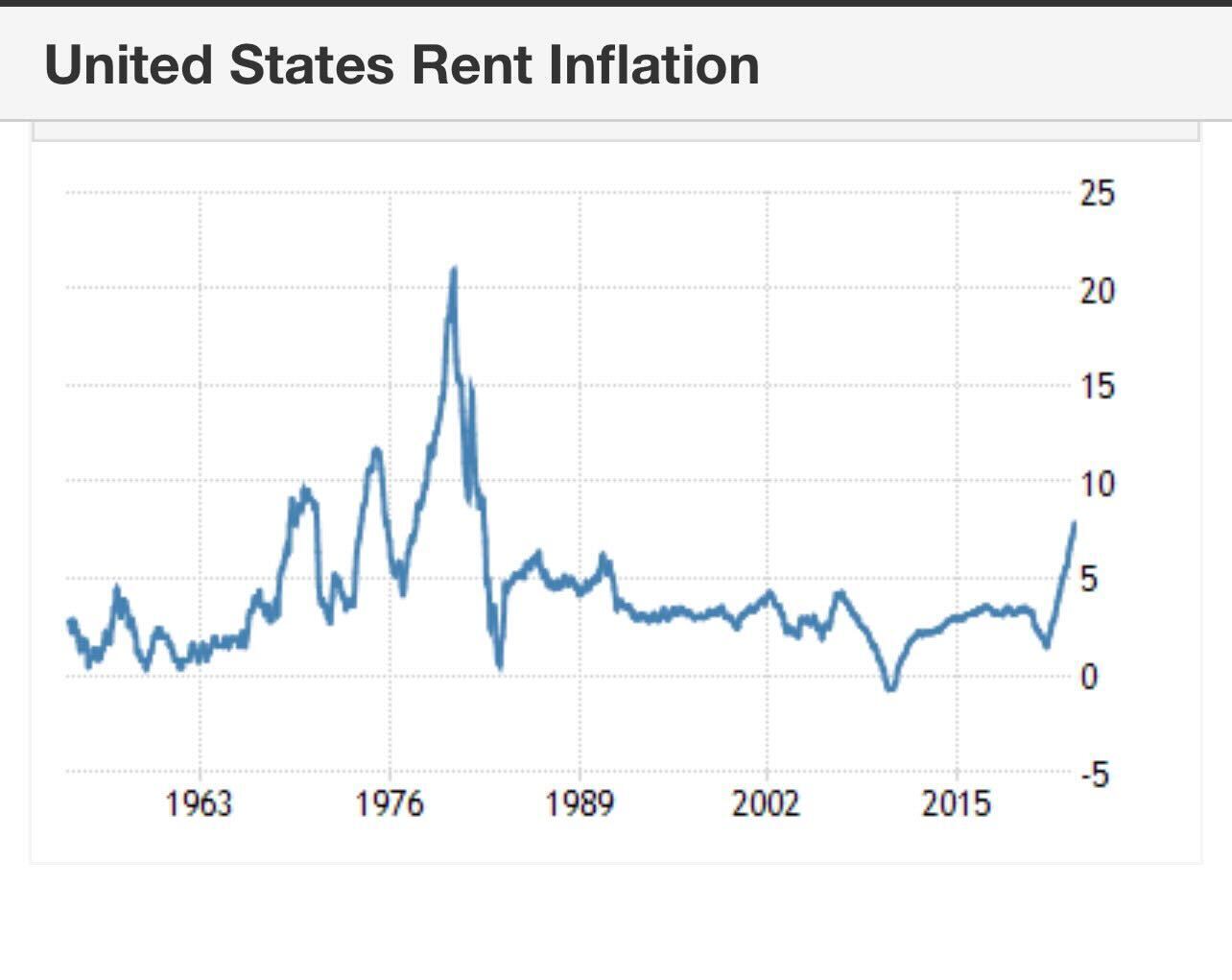

The Federal Reserve said it does not want the 1970s entrenched inflation. This means if you’re to think them, they’re afraid to death of a housing increase! In the 1970s, we observed a few leasing inflation booms, but the entrenched inflation in the mid to late 1970s is what they don’t want to see once more.

Even with the recession in 1974, inflation and charges grew, and in the late 1970s inflation and housing demand were being booming greater. I really do not consider they believe in this form of inflation, so they’re chatting about getting closer to the conclusion of their charge hikes.

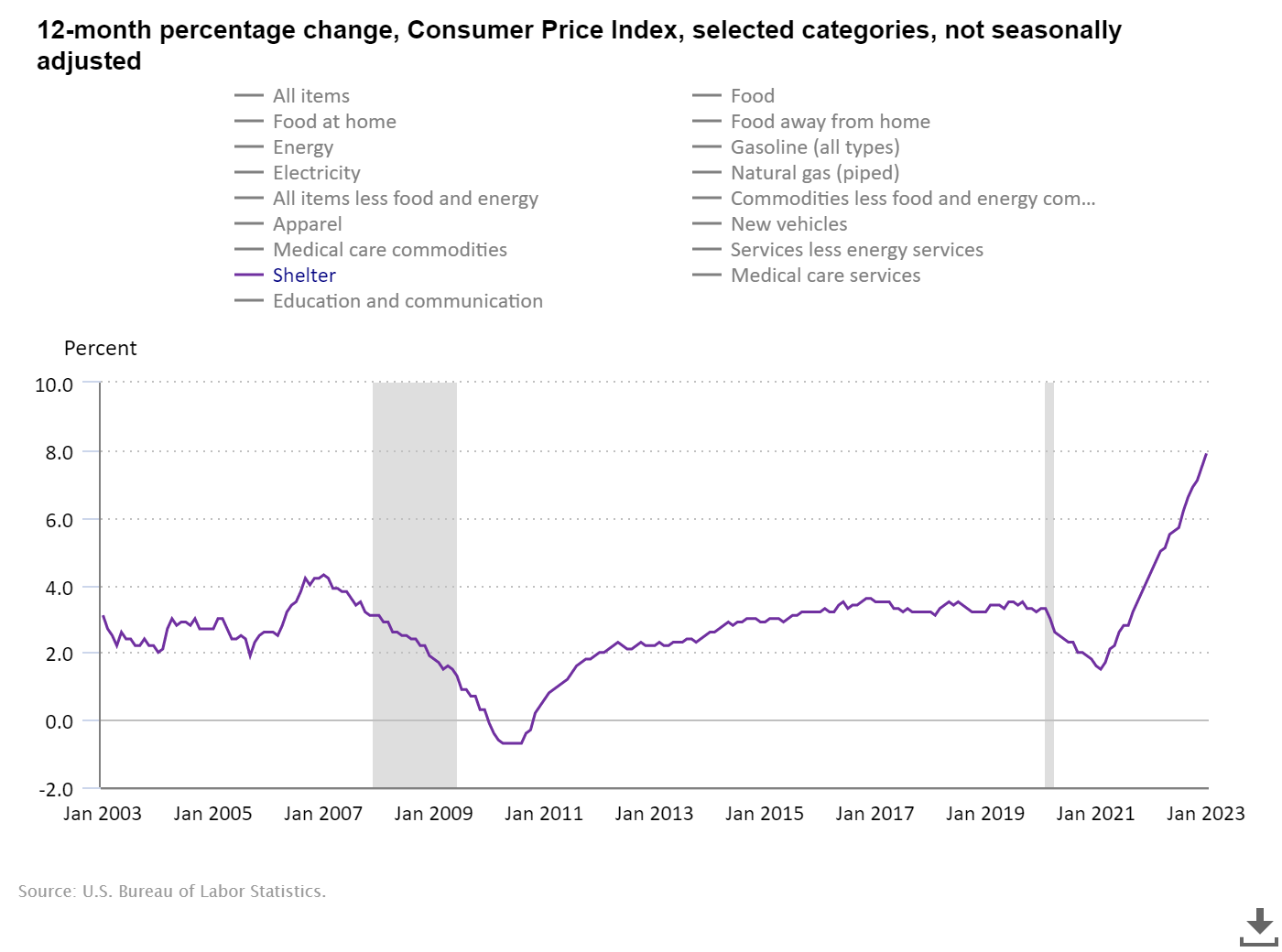

Since 43% of main CPI is shelter inflation, you can see why rents are so crucial. Right after the 1970s, the growth amount of inflation cooled off as lease inflation cooled off and was fairly secure up right up until the world wide pandemic, as you can see under, the calendar year-above-12 months inflation development price.

It is properly recognised now that the CPI hire inflation information lags terribly, and we are currently seeing the progress charge of hire cooldown, something I talked about on CNBC last September on CPI inflation working day.

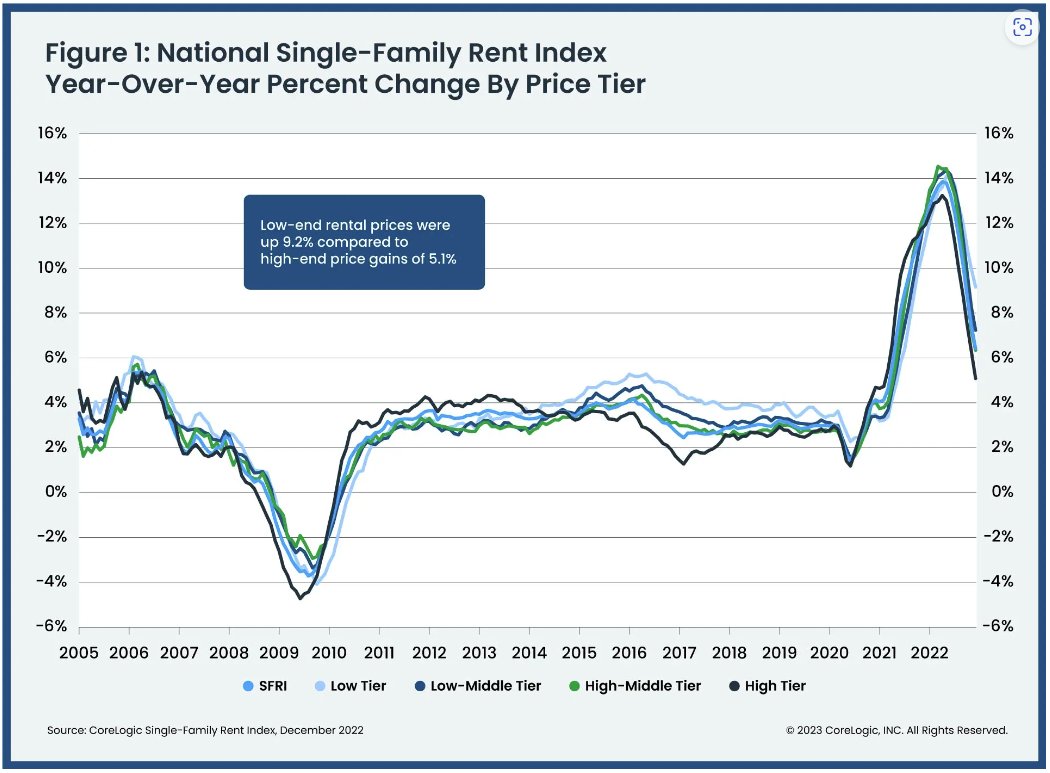

From CoreLogic:

Now glance at the shelter inflation details of CPI these days huge difference. To the Fed’s credit score, they did produce an inflation index to acquire shelter inflation absent from the discussion, which means they want to focus a lot more on provider inflation owing to the lag in lease inflation.

All over again, this is why I imagine they’re afraid of 1970s inflation, but they also know deep down inside, as the bond industry knows, we do not have the backdrop of 1970s inflation. I was not sure if they realized of the lag facet for a whilst there, but they resolved this by making their index in December that it does not depend housing inflation.

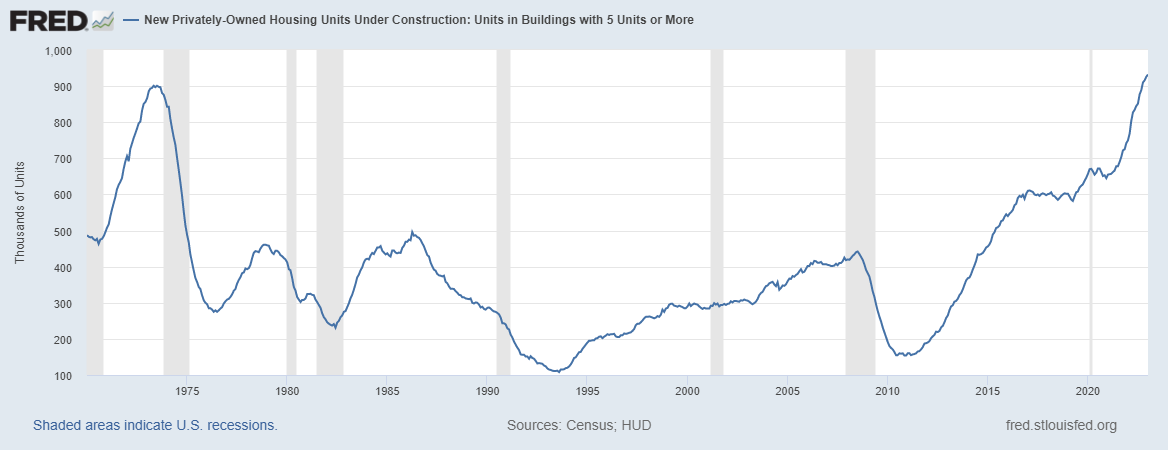

We have a history quantity of 5-unit development going on, so the most considerable component of CPI is by now slipping in serious conditions. We have a great supply coming on line, way too, with the Fed executing what it can to awesome the financial system down.

So the outlook is fantastic in this article on blocking a 1970s inflationary growth on hire growth. As we can see below, the 1974 economic downturn also killed the expansion of 5 models under design. This is not the case nowadays!

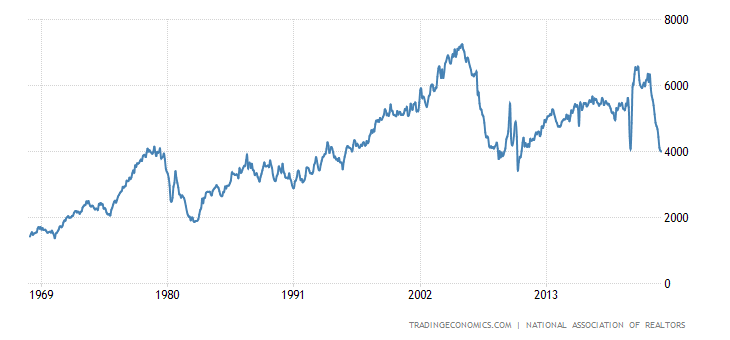

I have found recently that individuals don’t know how a great deal housing boomed again in the mid to late 1970s. Existing household income doubled in advance of we noticed the collapse in demand. We went from 2 million to 4 million and back to 2 million. We are not in the boom gross sales desire stage nowadays as present household revenue had the largest just one-yr regular income collapse.

So, although I am not a Fed pivot particular person until finally jobless promises break in excess of 323,000 on the four-7 days relocating average, I did have the peak 10-yr generate at 4.25% this 12 months with a 7.25% peak property finance loan price degree. I am not blinded to the actuality that inflation and progress have limitations as charges rise, with the source of 5-unit coming on line.

I imagine the bond current market has constantly recognized this, which is why the large inflation ranges, the 10-12 months generate, and mortgage loan premiums never seem like the 1970s right now.

Why would it be much less probable for home loan costs to rise from these degrees compared to why they would be a lot more probably to drop?

The growth charge of inflation is now cooling off, source chains are having far better, rental inflation will eventually catch up into the inflation info, furthermore we have additional offer of rental units coming on line. All these things stage to us not acquiring a 1970s redux.

It is getting from in this article to there that will have a good deal of financial noise and confusion, and the Fed doesn’t do by itself any favors when they communicate weekly and seem like they are confused about what to do.

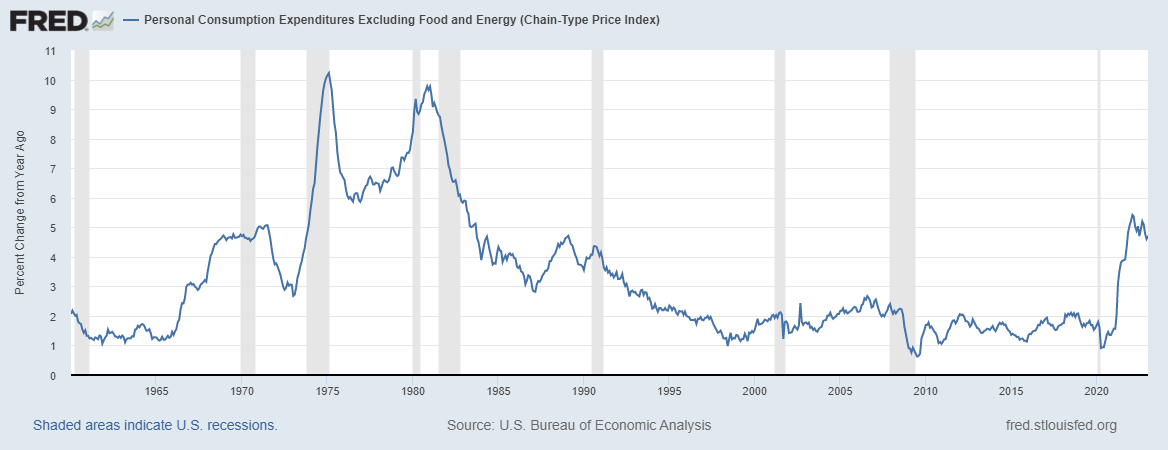

However, with that reported, we really should have a a few-cope with on the Main PCE development level of inflation by the close of the yr. Back again in the 1970s, this information line which is the Fed’s principal focus on level, was nearing 10%. Now it is at 4.7% and even the Fed’s forecast displays this slowing down by the stop of the 12 months.

Whilst we are not heading to hit the Fed’s goal of 2% calendar year-over-calendar year growth on inflation this calendar year, the development level of core PCE is slowing down now, which displays why the Fed and the bond market really don’t think we are going to get to 1970s-degree inflation.

We have a whole lot of sound about rates and inflation lately, and some persons say that to wipe out inflation, we require a more powerful-than-predicted task decline recession, such as we saw in the 1970s. Ideally, the info I showed you right now can put the 1970s to rest.

If your newborn boomer mates are concerned of the 1970s again, give them a hug and tell them almost everything will be alright we will endure this. Do not forget about that Fed charge hikes have a lag, simply because they have a lagging affect to the overall economy, the Fed really needs to end climbing before long, so they really do not have to reduce rates a lot quicker than they want.