Current household income experienced a huge defeat of estimates on Tuesday. This wasn’t stunning for persons who stick to how I monitor housing facts. To comprehend why we experienced this sort of a defeat in sales, you only will need to go again to Nov. 9, when house loan fees started out to tumble from 7.37% to 5.99%.

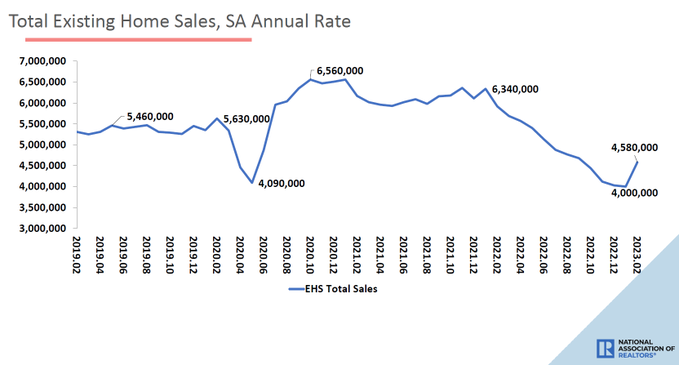

For the duration of November, December and January, invest in software facts trended constructive, indicating we had numerous months of much better-hunting knowledge. The weekly growth in purchase application information for the duration of those people months stabilized housing income to a historically lower amount.

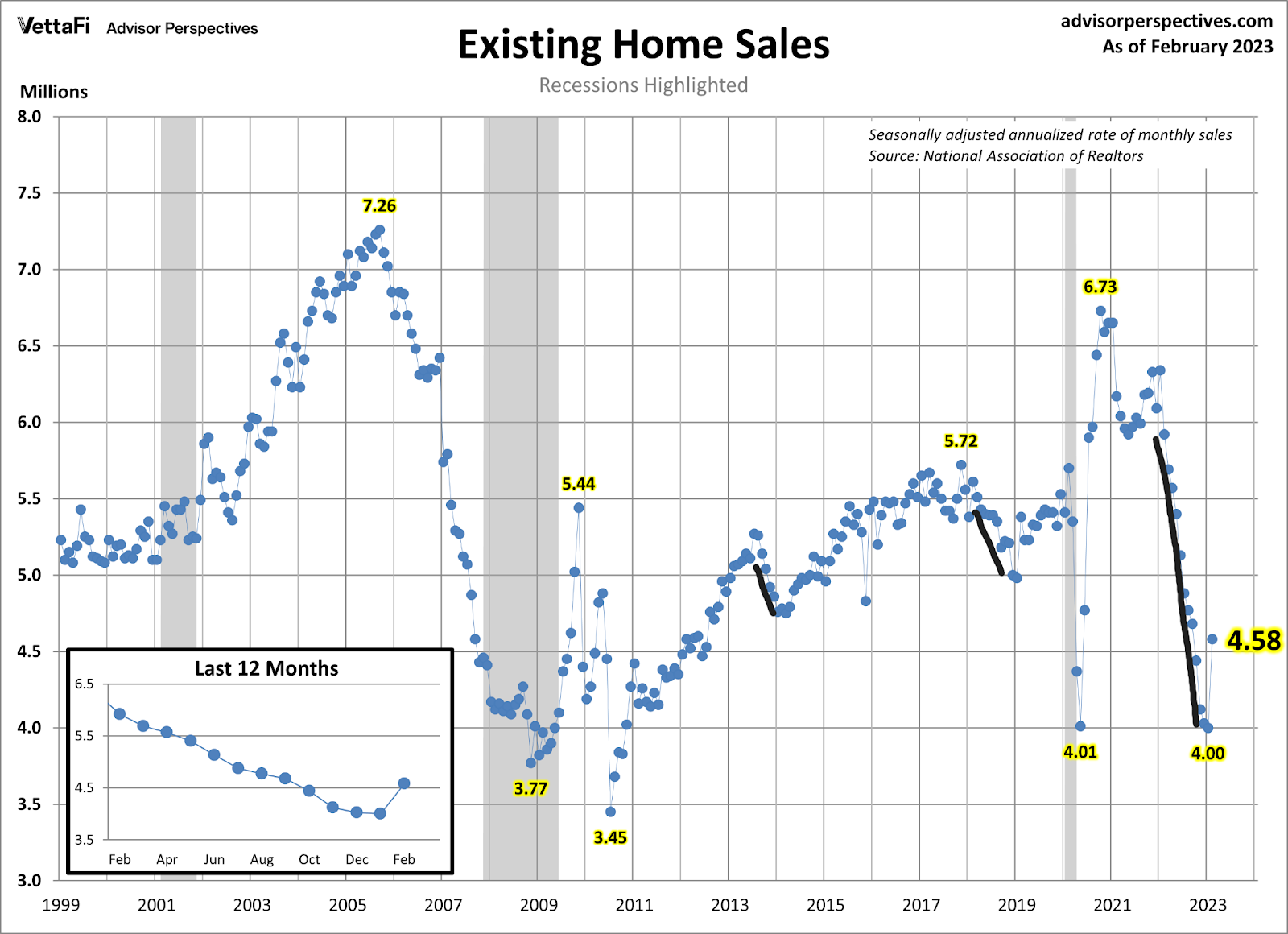

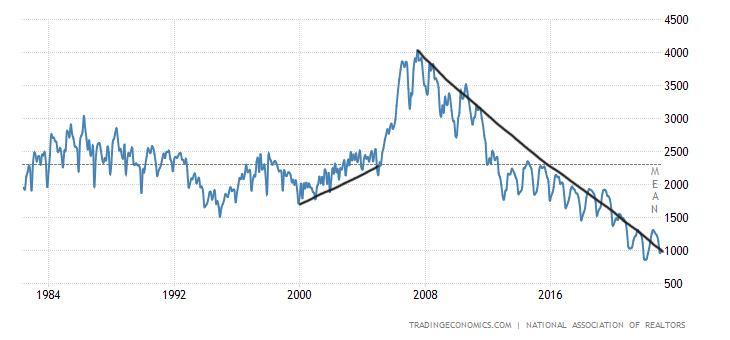

For a lot of decades I have talked about how rare it is that present home profits craze down below 4 million. That is why the historic collapse in demand in 2022 was one particular for the report books. We comprehended why product sales collapsed throughout COVID-19. Having said that, that was mostly owing to conduct changes, which intended gross sales were being poised to return greater once behavior returned to standard.

In 2022, it was all about affordability as mortgage loan prices had a historical rise. Lots of individuals just did not want to promote their properties and go with a much greater whole value for housing, even though 1st-time homebuyers experienced to deal with affordability difficulties.

Even even though property finance loan rates ended up falling in November and December, optimistic obtain software info takes 30-90 times to strike the revenue knowledge. So, as revenue collapsed from 6.5 million to 4 million in the month-to-month profits details, it set a small bar for sales to mature. This is a thing I talked about yesterday on CNBC, to just take this home sale in context to what happened in advance of it.

Mainly because housing information and all economics are so violent currently, we created the weekly Housing Sector Tracker, which is created to look ahead, not backward.

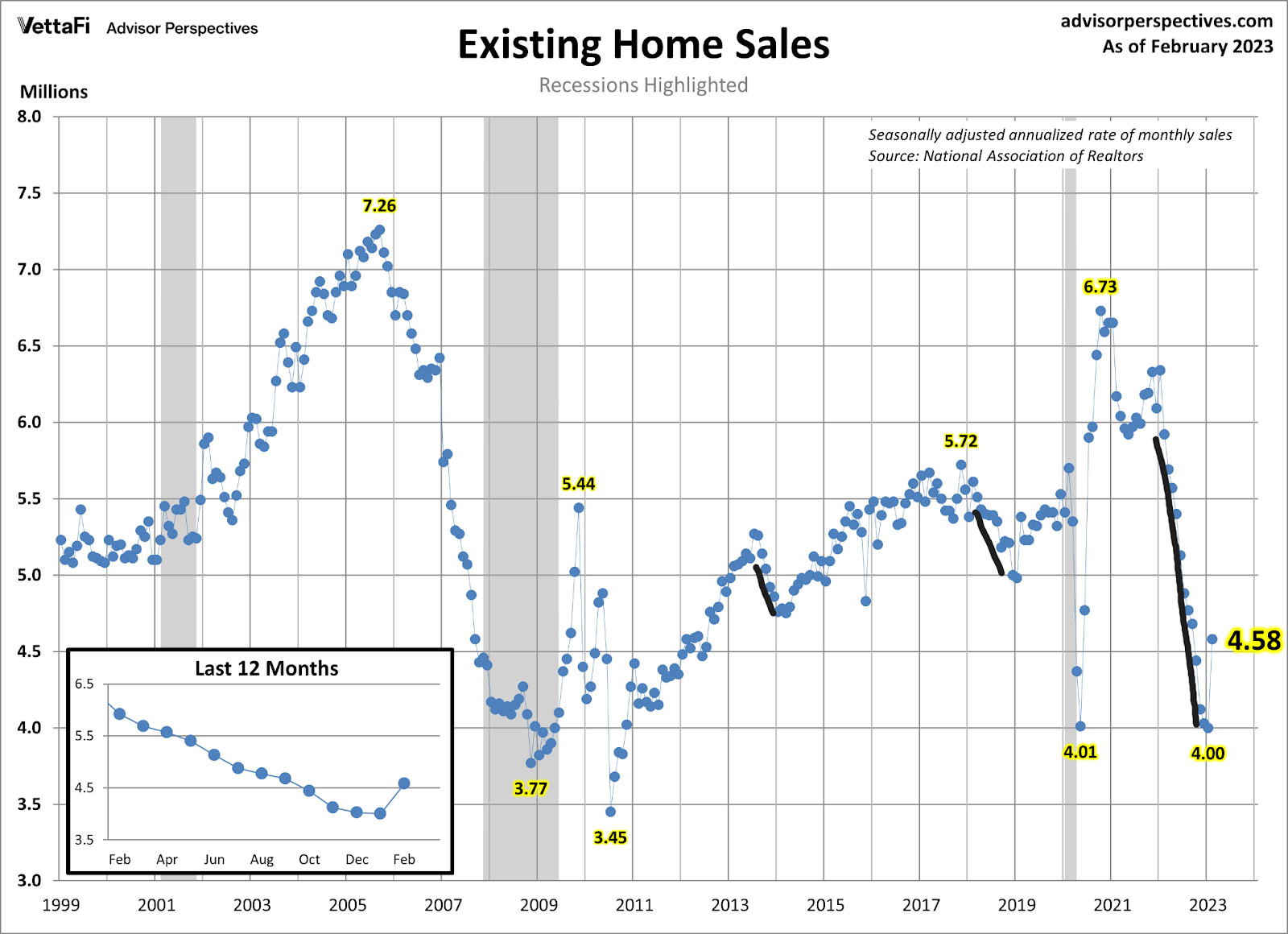

From NAR: Total existing-house profits – concluded transactions that consist of one-loved ones residences, townhomes, condominiums and co-ops – vaulted 14.5% from January to a seasonally adjusted once-a-year charge of 4.58 million in February. 12 months-in excess of-year, sales fell 22.6% (down from 5.92 million in February 2022).

As we can see in the chart over, the bounce is quite visible, but this is distinctive than the COVID-19 lows and substantial rebound in revenue. House loan prices spiked from 5.99% to 7.10% this yr, and that created a person month of detrimental ahead-wanting buy application knowledge, which requires about 30-90 times to strike the profits knowledge.

So this report is also old and sluggish, but if you comply with the tracker, you’re not gradual. This is the wild housing action I have talked about for some time and why the Housing Marketplace Tracker results in being handy in comprehension this facts.

The last two weeks have experienced optimistic order application facts as mortgage loan fees fell from 7.10% down to 6.55% tomorrow, we will see if we can make a third beneficial 7 days. 1 issue to try to remember about obtain application info because Nov. 9, 2022 is that it is experienced a good deal a lot more positive details than hazardous knowledge.

Nevertheless, the 1-month drop in obtain application info did provide us back to concentrations last viewed in 1995 not long ago. So, the bar is so small we can trip about.

A person of the reasons I took off the savagely unhealthy housing sector label was that the days on the sector are now previously mentioned 30 days. I am not endorsing, nor will I ever, a housing sector that has days on the marketplace at teenager stages. A teen amount signifies a single of two undesirable issues are taking place:

1. We have a substantial credit rating increase in housing which will blow up in time since demand is booming, comparable to the run-up in the housing bubble many years.

2. We simply really don’t have enough products for homebuyers, building pressured bidding in a very low-stock natural environment.

Guess which one we experienced post 2020? Glance at the invest in application details over — we in no way experienced a credit history boom. Glimpse at the Stock info below. Even with the collapse in home profits and the 1st serious rebound, total lively listings are continue to down below 1 million.

From NAR: Full housing stock registered at the end of February was 980,000 units, equivalent to January & up 15.3% from one year in the past (850,000). Unsold stock sits at a 2.6-month source at the present income speed, down 10.3% from January but up from 1.7 months in February ’22. #NAREHS

Nevertheless, with that said, the 1 data line that I like, enjoy, adore, the times on the marketplace, is above 30 times once again, and no for a longer time a teen like final calendar year, when the housing market place was savagely harmful.

From NAR: Initially-time buyers have been responsible for 27% of product sales in January Personal buyers acquired 18% of properties All-money revenue accounted for 28% of transactions Distressed sales represented 2% of sales Houses ordinarily remained on the sector for 34 days.

Today’s current property product sales report was very good: we saw a bounce in gross sales, as to be anticipated, and the days on the market are nevertheless more than 30 days. When the Federal Reserve talks about a housing reset, they’re declaring they did not like the bidding wars they observed previous calendar year, so the simple fact that cost progress appears to be practically nothing like it was a calendar year in the past is a excellent issue.

Also, the days on market place are on a level they may possibly feel additional relaxed in. And, in this report, we noticed no symptoms of pressured marketing. I’ve usually thought we would never ever see the forced marketing we saw from 2005-2008, which was the worst portion of the housing bubble crash years. The Federal Reserve also thinks this to be the scenario simply because of the better credit score standards we have in position since 2010.

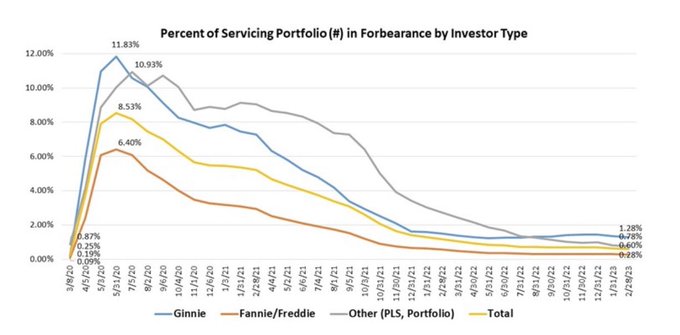

Case in level, the MBA‘s modern forbearance info exhibits that as an alternative of forbearance skyrocketing greater, it is collapsed. Recall, if you see a forbearance crash bro, hug them, they have to have it.

Today’s existing dwelling profits report is backward wanting as acquire application data did just take a strike this 12 months when home loan fees spiked up to 7.10%. We all can agree now that even with a massive collapse in revenue, the stock details didn’t explode bigger like numerous have predicted for over a decade now.

I have pressured that to understand the housing market, you need to have an understanding of how credit score channels function post-2010. The 2005 individual bankruptcy reform laws and 2010 QM laws transformed the landscape for housing economics in a way that even right now I do not feel folks have an understanding of.

However, the housing current market took its most significant shot ever in phrases of affordability in 2022 and so far in 2023, and the American home-owner did not stress when. Even nevertheless this details is aged, it exhibits the stable footing householders in The united states have, and how poorly completely wrong the particularly bearish individuals in this place were being about the state of the financial affliction of the American property owner.