I referenced in my last belief piece in Housing Wire that the Urban Institute publishes a “monthly chart book” that is packed total of suitable info. This recent publication paints a obvious photo as to why any Realtor or homebuilder need to generally incorporate a nonbank financial institution in their referrals.

Prior to I open up myself up to attacks here, I am utilizing macro info from Urban Institute and there are undoubtedly some banking companies who provide a broader swath of the current market. But let us start off with the basics as to who genuinely is increasing credit score accessibility in the sector.

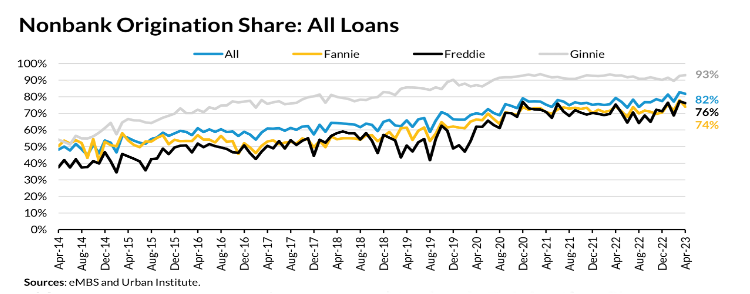

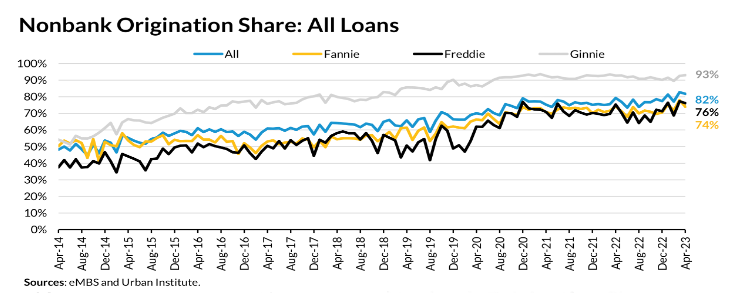

When on the lookout at the nonbank share of all financial loans broken down by trader (Fannie, Freddie, and Ginnie Mae) the obvious info level that stands out is that nonbanks do properly more than 80% of all financial loans currently being manufactured these days. Far more importantly, when it arrives to the Ginnie Mae plans, banking institutions contribute only 7% of all the mortgages by the FHA, VA, and USDA. 7 per cent is a obvious determine, in particular when you appear at the dynamics shaping the housing current market.

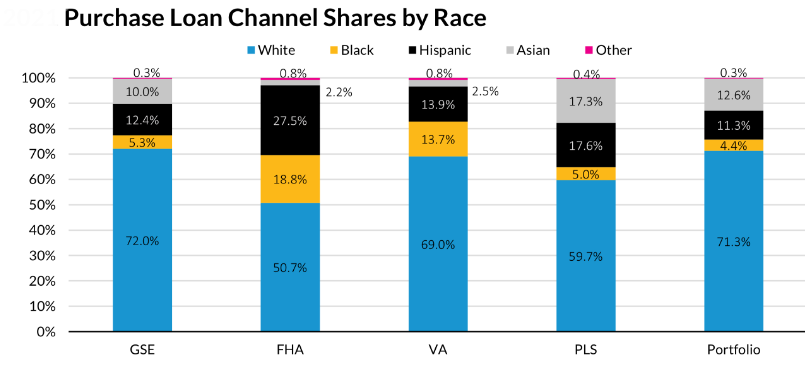

The cause why this stands out is that the distribution of financial loans in the Ginnie Mae programs has the highest concentration of initially-time homebuyers and the biggest proportion of minorities. In the FHA application by yourself, 46.3% of all financial loans are to Hispanic and Black debtors and with about 80% of all FHA’s purchase transactions likely to initially-time homebuyers, the simple fact that financial institutions only do 7% of these financial loans is amazing.

Why does this all issue? For the reason that the important regulators in Washington commit a lot of their time ingratiating themselves to the banking marketplace and lamenting about nonbanks. As Chris Whalen articulated in his the latest op-ed, “Consumer Money Security Bureau head Rohit Chopra said in Might that ‘a main disruption or failure of a substantial home loan servicer really presents me a nightmare.’ He produced these intemperate opinions throughout CBA Reside 2023, a convention hosted by the Consumer Bankers Affiliation.”

The fact that regulators commit time “biting the hand that feeds them,” my reference to the point that it is the nonbanks giving assistance for the constituency that this administration should care about and surely not the audience at a CBA convention, is really alarming.

As Whalen goes on to highlight, “Chopra’s concentrate is political rather than on any serious menace. But of system, progressive alternatives require problems. 3 large and mismanaged depositories unsuccessful in the initial quarter of 2023, but progressive partisans like Chopra, Treasury Secretary Janet Yellen, and Federal Housing Finance Company head Sandra Thompson ignore the general public file and continue to fret about nonexistent risk of contagion from house loan servicers.”

I have taken a whole lot of adverse feedback from quite a few who are connected to the current administration about my criticism of things like LLPA price adjustments. But in a very similar context as Whalen, I am tiring of the politics of an administration and its regulators who emphasis their time on making an attempt to reign in the independent property finance loan financial institutions (IMBs) — the quite set of establishments that are responsible for making certain that accessibility to credit history remains for American families who may possibly or else be shut out of the current market.

1 may question, why do IMBs do so substantially superior listed here in advancing credit rating availability? I imagine it will come down to a core principal: IMBs only do mortgages. Unlike banking companies, they really don’t do automobile financial loans, credit playing cards, university student loans, company lending, traces of credit and more. Banking institutions don’t need to have to broaden their home finance loan lending firms. In truth, the craze has been to retreat from mortgages, not embrace this phase more.

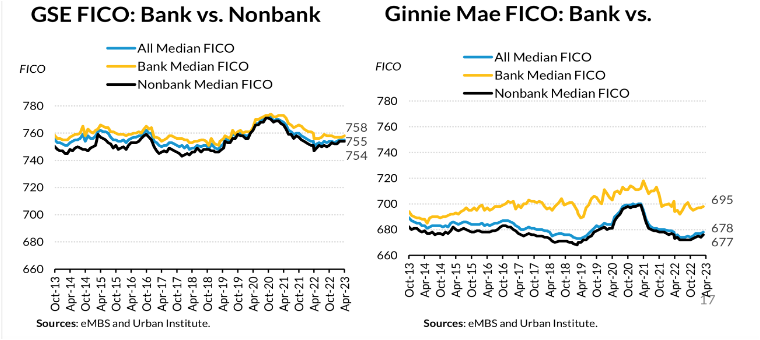

Just seem at the knowledge. When it comes to credit rating (FICO) scores, IMBs are drastically much more aggressive. And given that credit rating scores are lessen for to start with-time homebuyers and pattern reduced in most minority segments, the IMBs by natural means prevail as the most effective possibility for the homebuyer.

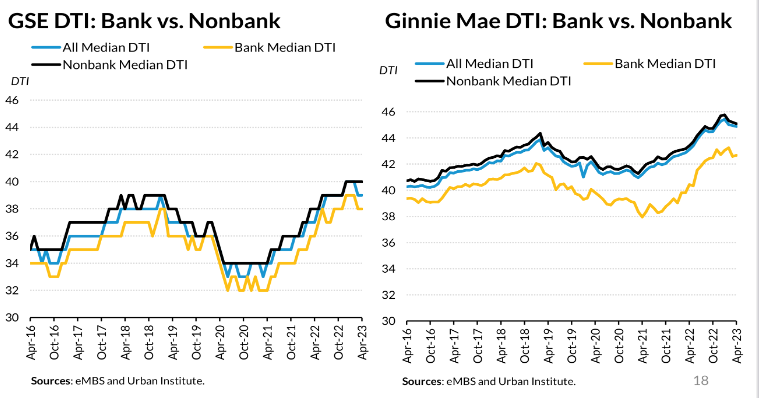

Or glimpse at this information on DTI (financial debt to cash flow ratio). The spread involving median lender DTIs compared to nonbanks in the Ginnie Mae plan is important and, frankly, will influence these on the margin of access to homeownership in a important way.

The fact that banks are only 7% of all Ginnie Mae lending is not by accident. The fact is that they have systematically walked absent from any element of property finance loan lending that would seem to be of better threat. It’s frankly why businesses like Wells Fargo currently are a shadow of the mega-current market dominators that they after were being.

Whalen most likely explained it most effective stating, “More than any genuine-planet dilemma posed by IMBs, it is the authorities in all of its manifestations that poses a important danger to the earth of home finance loan finance and the housing sector extra normally. Washington regulatory organizations find to stifle the marketplaces, restrict liquidity and impose added money principles, strictures that need to inevitably lower financial development and entry to reasonably priced housing.”

We have a labyrinth of federal regulators who failed to see how the considerable rise in banks’ cost of funds, driven by the steps of the Federal Reserve, may force some banks into detrimental foundation territory. This situation, where by they have been shelling out depositors more than they ended up earning on their unhedged property, set them out of business. And the regulators skipped all of this. In all of their angst and speech-making about the risks of nonbanks, they just disregarded three of the most expensive failures in banking record.

As I publish this, I know that I far too was once component of the vanity of an administration that lectured and directed far more than it listened at occasions. But today we encounter as well numerous challenges. Whalen plainly articulates how the GSEs are becoming directed down a path that will only lower their relevance over time if still left unchecked.

But probably the core concept in this article is this: If I had been a Real estate agent or homebuilder, I would make sure that my opportunity buyers, in particular my initial-time homebuyers, ended up in conversation with an IMB (or mortgage broker). If that simple move isn’t being done, then the accessibility to credit score difficulties will very likely only loom more substantial.

Try to remember, IMBs are not risk having entities. They go by means of the credit rating chance into government-backed lending institutions and they get paid out a payment to provider the loans for these government entities. We have to have regulators to cease speechmaking at banking conferences about possibility listed here and in its place applaud the significant part these companies carry out.

A lot more importantly, regulators must commit a lot more time bolstering types of liquidity to these entities. There are answers that can assistance.

But really, the much more time they commit politicizing the nonbank story, we possibility extra lender failures, which are genuinely the larger risk in the sector. Let us applaud the IMBs for holding the doorways to homeownership open. And let us demand from customers that our regulators end using political platforms to distort others’ sights when not focusing on their most important responsibilities.

Accountability will only exist when stakeholders demand it.

David Stevens has held several positions in real estate finance, which includes serving as senior vice president of single loved ones at Freddie Mac, government vice president at Wells Fargo Home Home loan, assistant secretary of Housing and FHA Commissioner, and CEO of the House loan Bankers Association.

This column does not necessarily replicate the opinion of HousingWire’s editorial division and its owners.

To call the creator of this story:

Dave Stevens at [email protected]

To call the editor accountable for this tale:

Sarah Wheeler at [email protected]