Previous June, the Federal Reserve said it preferred a housing reset, which meant it preferred increased house loan charges to destroy the housing industry. This facilitated the greatest drop in current household product sales for a single year that we will ever see in modern day-working day record due to the superior degree of sales in January of 2022.

Currently, the Federal Reserve achieved its key goal the times on the marketplace are now over 30 days, which was the most significant data line to get housing back to to some degree standard. Of course, this place the housing industry into a economic downturn on June 16, 2022.

Currently I am a satisfied camper due to the fact very last calendar year, the housing current market was savagely unhealthy with days on the marketplace in the teens, and now we are again to a regular stage above 30 times. We cannot have a performing housing market place with times on the marketplace beneath 20 times.

Two horrible points could clarify why the times on the current market are underneath 20 days. No. 1, a massive credit housing bubble in demand, which will pop ultimately. Of study course, we never have that now. Having said that, the 2nd is that stock is basically also lower, with as well numerous people chasing as well number of houses, which suggests far too a lot of bidding wars. We are not obtaining bidding wars like we saw when the times on the market were under 20 days.

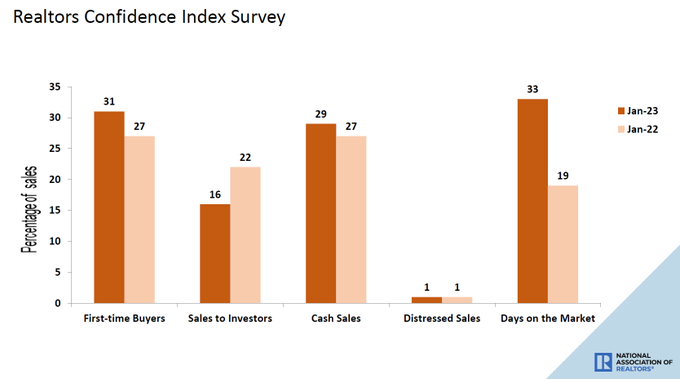

NAR Investigation: Initial-time buyers ended up accountable for 31% of sales in January Personal buyers acquired 16% of properties All-money product sales accounted for 29% of transactions Distressed revenue represented 1% of revenue Homes commonly remained on the industry for 33 times.

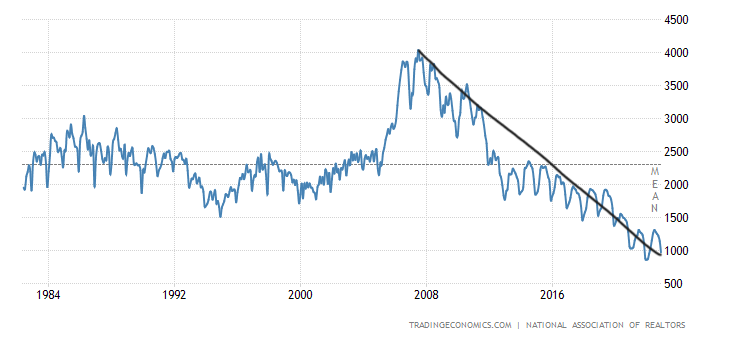

My problem for 2020-2024 has been that inventory degrees could break to all-time lows, which suggests even if sales ended up trending related to the past growth, we basically have too quite a few people chasing much too couple residences. The bidding wars you listened to about this 12 months weren’t mainly because of document-breaking desire but for the reason that lively listings are still close to all-time lows. The full stock these days is however beneath 1 million at 980,000.

Inventory is greater this calendar year than final, but I will jump for pleasure again if we can just strike 1.52 million. This would give the housing sector a buffer in offer, just in scenario mortgage premiums slide once more. This didn’t happen this yr, so we hear stories of bidding wars again early on in areas of the U.S. that do not have stock around 2019 stages.

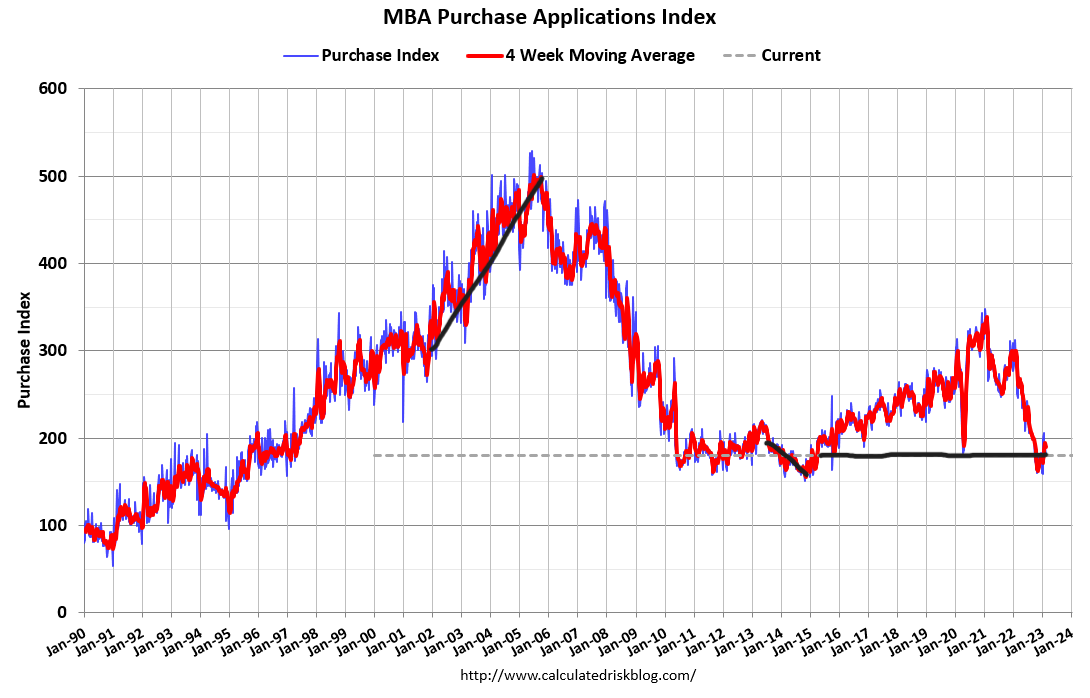

This is why previous 7 days on CNBC, I cautioned men and women to be conscious when speaking about housing booming all over again. Ahead-looking obtain apps have risen from a waterfall dive, and we have witnessed the data stabilize. We will bounce from this degree, but context issues.

This is why we established the Housing Sector Tracker: facts moves incredibly fast, and now that house loan fees have spiked up again, we need to track to see how significantly injury better charges do to need.

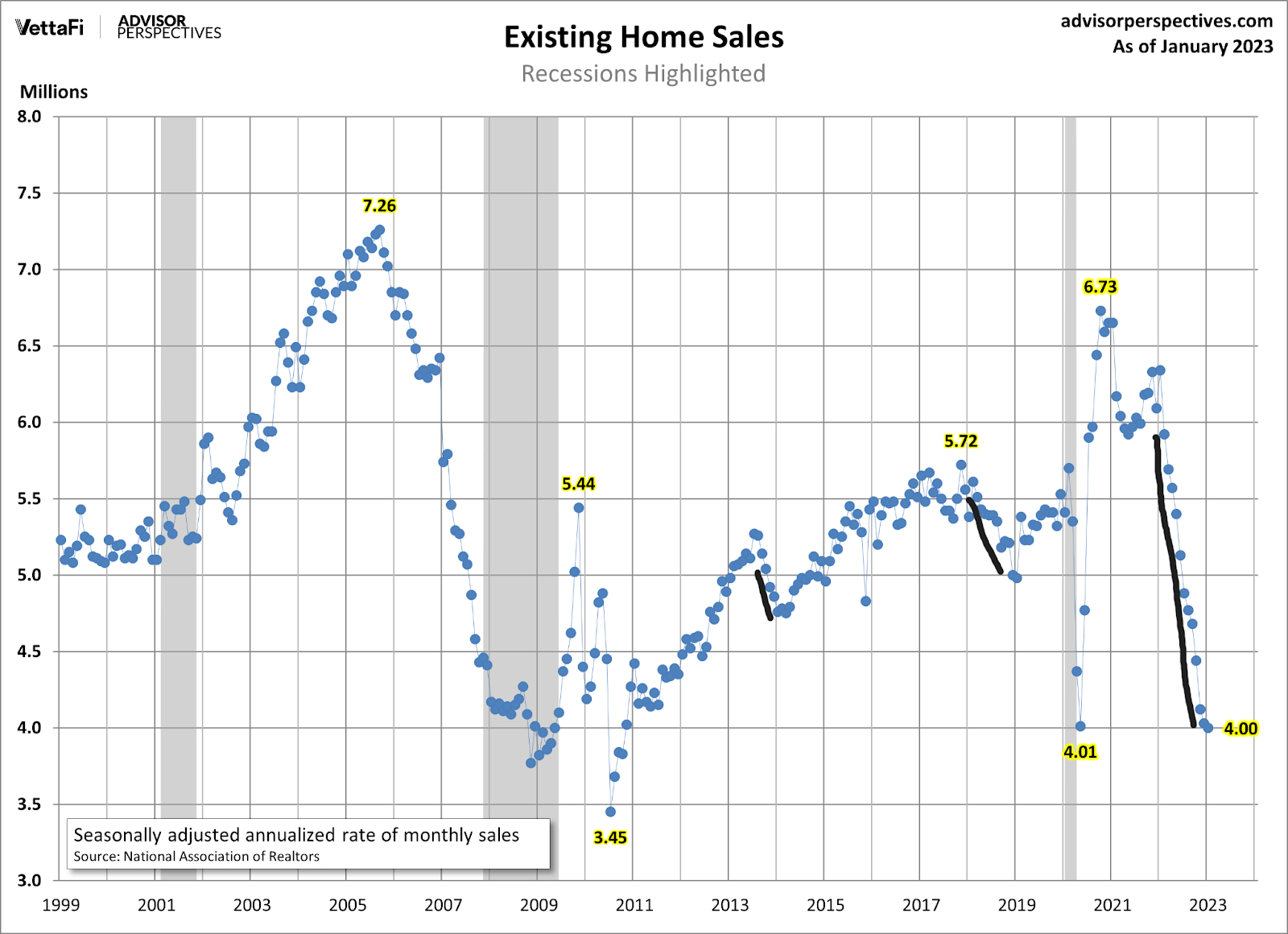

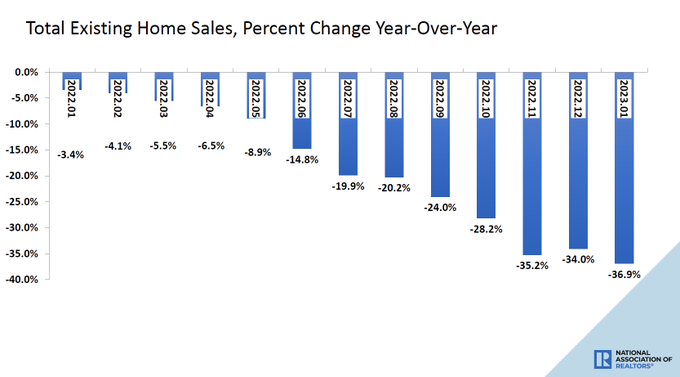

NAR: Overall existing-home profits: done transactions that contain single-loved ones residences, townhomes, condominiums and co-ops, slid .7% from December 2022 to a seasonally modified once-a-year amount of 4.00 million in January. 12 months-around-yr, revenue retreated 36.9% (down from 6.34 million in January 2022).

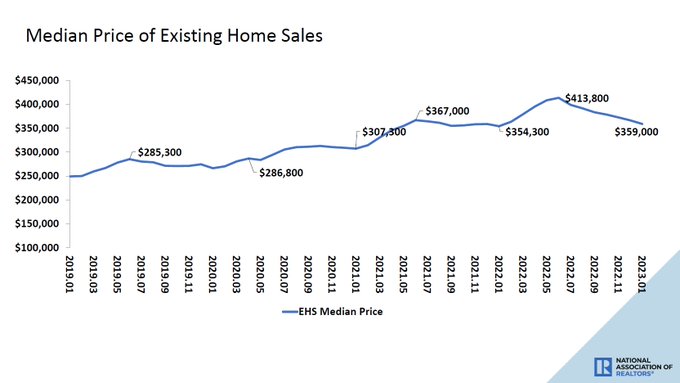

“Home profits are bottoming out,” claimed NAR Main Economist Lawrence Yun. “Prices fluctuate depending on a market’s affordability, with lower-priced regions witnessing modest advancement and extra costly locations encountering declines.”

A person of the ahead-looking data line points I have talked over due to the fact Nov. 9 is that housing need enhanced with purchase applications, so the worst sales declines are about. Nonetheless, the income knowledge won’t demonstrate that enhancement right up until February or March of this 12 months, which means the January and February current house sales stories.

Acquire software details is forward-looking 30-90 days, so it takes some time for much better demand from customers to strike the existing property profits report. On the other hand, it’s apparent that the major main declines we observed in product sales in the 2nd fifty percent of 2022 have settled down

Of program, this means we need to have to observe ahead-on the lookout knowledge, as better home finance loan prices must sluggish the housing market place. The housing marketplace can nevertheless be quite frustrating to buyers and sellers because property finance loan prices can transfer quickly up or down. Since the close of June very last yr, when premiums went higher than 6%, new listing details has declined, and this final 7 days we strike a weekly new all-time very low for the former week.

- 2019 – 65,868

- 2020 – 62,447

- 2021 – 50,671

- 2022 – 49,159

- 2023 – 42,769

- This is not a great tale for housing mainly because a conventional seller is ordinarily a traditional consumer. So, if individuals do not listing their households to offer and obtain, need can collapse, as we saw in 2022.

As you can see beneath, the calendar year-about-12 months declines are large, but as the calendar year progresses, the declines should get significantly less if demand from customers is stable from these amounts, specifically in the 2nd half of 2023.

NAR Investigate: Yr-above-year, revenue retreated 36.9% (down from 6.34 million in January 2022).

Value progress has cooled substantially, particularly in the 2nd half of 2022. As someone who claimed we needed better charges in February of 2021 and deemed the housing industry savagely unhealthy in February 2022, this puts a smile on my experience.

NAR Investigation: The median current-household selling price for all housing varieties in January was $359,000, an raise of 1.3% from January 2022 ($354,300), as price ranges climbed in a few out of 4 U.S. areas when falling in the West.

My panic since 2020 has always been that we would have key housing inflationary difficulties if stock broke to all-time lows all through 2020-2024. Of training course, this happened, and then some, in the most destructive vogue at any time.

My rule of thumb for 2020-2024 was that if house rates grew 23% for the duration of these 5 many years, we would be okay with housing. This, of class, didn’t come about, as residence charges grew 30% in just 2020-2021, and at the time premiums rose in 2022 soon after the key housing inflation hit, demand from customers just collapsed.

Nevertheless, with that reported, the one matter I needed to see to get again to a unexciting and well balanced current market ultimately happened right now: days on the market bought in excess of 30 times.

This is a massive phase in finding back to normal, even even though I know my forecast last June of just obtaining complete housing stock back to 2019 degrees — which usually means just breaking above 1.52 million — looks poor now. Nevertheless, just one of the aspects for this to occur was to have days on the sector get above 30 days once more. This is a good action in the ideal course.