The housing current market capabilities in another way than other markets for the reason that it can be characterised as a heterogeneous, thinly traded, illiquid sector. In other words and phrases, it’s a numerous industry with a extensive selection of distinctive properties of varying ages and levels of repair service, and sales occur pretty almost never.

And there’s an additional matter that separates the housing industry from other marketplaces — the consumer is generally also the vendor. In most markets, the vendor, or provider, makes their determination about incorporating supply to the industry unbiased of the purchaser, or source of need, and their determination to buy. In the housing current market, the seller and the buyer are, in several conditions, the exact economic actor.

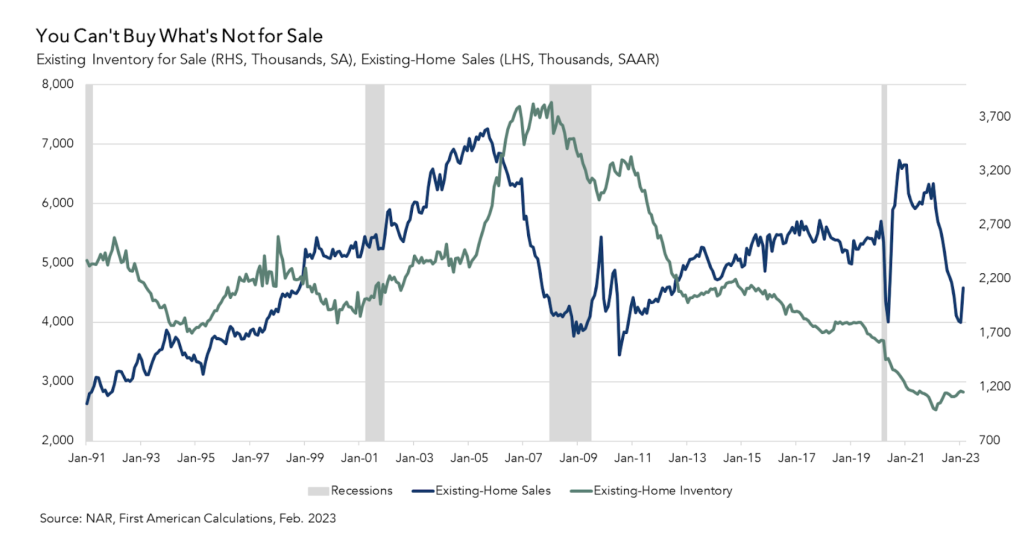

To purchase a new residence, you will have to offer the property you now own. From the year 2000 right until the begin of the pandemic in 2020, present-household stock built up virtually 90% of total dwelling inventory. And, regrettably, sellers are not offering in today’s better property finance loan rate environment. The most important element holding back today’s housing sector is not lack of demand from customers, but a dearth of source.

The golden handcuffs of very low home finance loan rates retain sellers level-locked in

Ahead of the housing current market crash in 2007, the typical duration of time anyone lived in their residence, or tenure, was somewhere around 5 several years. Normal tenure length grew to around 8 a long time during the aftermath of the housing sector disaster amongst 2008 and 2016. Given that then, tenure has further amplified to a historic substantial of 10.7 several years in March 2023, in accordance to recent info.

The golden handcuffs of reduced mortgage loan charges are locking several householders in place, particularly individuals who refinanced into rock-base mortgage loan fees more than the course of the pandemic. According to the hottest second quarter 2022 National Mortgage loan Databases knowledge, 92% of excellent home loans have charges underneath 6% and nearly 83% have a price under 5%. As extensive as the average 30-12 months, set mortgage amount continues to be higher, there is a economic disincentive for home owners to promote their present residences only to purchase their following residence at a better amount.

Of study course, the less households there are for sale, the more durable it gets to be to find a home that is improved than the dwelling you already possess. The fee “lock-in” effect stops far more housing supply from reaching the current market and lessens the skill to locate a residence you might want to buy. The result is less revenue.

This write-up is portion of our ongoing 2023 Housing Current market Forecast series. Soon after this collection wraps, join us on Might 30 for the next Housing Sector Update Party. Bringing with each other some of the leading economists and scientists in housing, the celebration will supply an in-depth glance at the top predictions for this yr, together with a roundtable dialogue on how these insights utilize to your business enterprise. To sign up, go in this article.

…But some could have the fairness to split totally free

It’s not likely that property finance loan rates will drop below 5% shortly, that means numerous current owners will continue to be monetarily disincentivized from advertising their property. Even so, there is one variable that could partly offset the influence of greater rates — fairness. Nationally, property rates greater far more than 40% from February 2020 (pre-pandemic) to the peak in June 2022.

Whilst prices have since declined nearly 3% from that peak, considerably of the house owner fairness acquired for the duration of the pandemic remains. Large stages of home equity could mitigate the impression of the charge lock-in effect by allowing sellers to place a much larger down payment on their new residence, serving to offset the impact of increased fees.

In other text, for some equity-abundant homeowners, transferring and getting on a higher curiosity level isn’t a large deal, in particular if they are transferring to a far more very affordable location. Probably more importantly, 42% of householders have no home finance loan at all, so they are totally absolutely free from the lock-in result.

Homer Simpson or Spock?

The scarcity of households on the market place proceeds to stifle property revenue. The recreation of musical chairs that is the housing current market requirements much more chairs. Sadly, with sellers currently being monetarily disincentivized to offer, it will possible set a ceiling on any raise in housing offer this year.

But there are mitigating elements, this kind of as fairness-wealthy and house loan-absolutely free home owners, that could offset some of the influence from bigger prices. And, of training course, there are lifestyle factors that travel the conclusion to provide that can sometimes outweigh the fiscal realities. As Nobel Prize winner Richard H. Thaler as soon as famously reported, we are much more like Homer Simpson than we are like Spock.

This column does not always reflect the feeling of HousingWire’s editorial office and its entrepreneurs.

To speak to the editor accountable for this story:

Mark Fleming at @mflemingecon (Twitter)

To get hold of the editor dependable for this story:

Brena Nath at [email protected]